Article page checkbox is not checked in page info.

Free allocation in the EU emissions trading system

Free allocation in the EU emissions trading system

Juan Fernando López Hernández, Members' Research Service

Summary

Since the establishment of the European emissions trading system (EU ETS), industrial installations exposed to the risk of carbon leakage have received free emission allowances for part of their greenhouse gas emissions. The EU ETS Directive provides for this percentage to be progressively reduced over the years in such a way that the EU ETS still provides a carbon price signal for decarbonisation and protects against the risk of carbon leakage. The EU has adopted a carbon border adjustment mechanism (CBAM) to replace the existing system of free allocation. The CBAM aims to ensure that imported goods are subject to the same carbon costs as those produced within the EU. However, the CBAM is still being phased in, and it does not cover all sectors exposed to the risk of carbon leakage.

The European Commission will propose a revision of the EU ETS in July 2026. The revision would re-define the role of the EU ETS post-2030, reinforcing it as an instrument that supports decarbonisation and industrial competitiveness. There are multiple issues at stake, but free allocation is expected to play a pivotal role in the discussion. Beforehand, the adoption of the Benchmark Regulation – the implementing act setting the revised values for free allocation of emission allowances – will establish the amount of free allocation to be granted in 2026-2030 to the sectors and subsectors in the EU ETS that are exposed to the genuine risk of carbon leakage. A broader revision of Directive 2003/87/EC on the EU ETS will begin afterwards, with a Commission proposal looking, among other things, at the role of carbon leakage in the EU ETS post-2030. This briefing provides an overview of the existing legislative framework and concepts related to free allocation in the existing EU ETS, and presents the views expressed by some Member States and stakeholders.

Free allocation in the EU ETS

The EU ETS is the cornerstone of the EU's climate policy. In 2025, it contributed to reducing ETS-covered emissions by more than half compared to their 2005 level, remaining well on track to meet its target of cutting greenhouse gas (GHG) emissions by 62 % in 2030. The EU ETS upholds the 'polluter pays' principle, requiring participants to pay for their carbon footprint. To comply with their emission obligations, participants must obtain emission allowances (certified rights to emit). Since 2013, auctioning has been the default method of allocating these allowances under the EU ETS. Through auctions, participants can buy the allowances they need for compliance.1 Auctioning is an important source of income, as Member States collect revenues from ETS auctions that they can later invest in climate and energy-related activities. Between 2013 and 2025, the EU ETS generated more than €258 billion in auction revenues.

A cross-sectoral correction factor safeguarding the 57 % auctioning share

The cross-sectoral correction factor (CSCF) is a safeguard instrument provided for in the EU ETS Directive that limits the total amount of free allowances available to industrial sectors. The CSCF is triggered when the demand for free allocation exceeds the amount available after the 57 % auctioning share required by the EU ETS Directive has been taken into account. When the aggregate preliminary free allocation calculated by Member States exceeds the maximum amount available for free allocation, the CSCF reduces the free allowances for all installations by the same proportion. In 2013, the CSCF was set at 94.27 % of the preliminary free allocation. The factor was later reduced each year, reaching 78.01 % in 2020 following a 2017 adjustment resulting from a judgment of the Court of Justice of the European Union. The application of the CSCF is estimated to have reduced free allocation to industry by close to 14 % on average between 2013 and 2020.

For the 2021-2025 sub-period of Phase IV of the EU ETS, the CSCF is set at 100 % CSCF, meaning that it does not further reduce the volume of free allocation. Following the revision of the EU ETS Directive in 2018, an additional buffer equivalent to 3 % of the total quantity of allowances may be used, if necessary, to avoid triggering the CSCF. This buffer will remain available during the 2026-2030 sub-period. The 10 % most GHG-efficient installations within each benchmark are exempt from any reduction in free allocation resulting from the triggering of the CSCF.

Eligibility for free allocation and exposure to the risk of carbon leakage

In principle, all industrial installations covered by the EU ETS, except those producing electricity only (with the exception of electricity produced from waste gases) and municipal waste incinerators, are eligible for free allocation2. To receive free allocation, installations must apply to their national competent authorities before the relevant deadline and be included in the national implementation measures list (NIMs)3. The NIMs are lists prepared by Member States detailing the preliminary amount of free allowances allocated to each installation and submitted to the Commission.

The EU ETS Directive establishes different levels of exposure to carbon leakage for the industrial sectors and subsectors it covers. These levels of exposure are important as they determine the level of free allocation to which a sector or subsector is entitled to receive. Article 10b of the EU ETS Directive establishes the conditions for a sector and subsector to be considered at risk of carbon leakage.

Understanding the concept of sector and subsector in the EU ETS

The EU ETS Directive requires the European Commission to publish a list of sectors and subsectors at risk of carbon leakage. The assessment can be carried out at the level of economic activity (using the Statistical classification of economic activities in the European Community (NACE)) or at product level (using Prodcom, the community production system of statistics on manufactured products). Both classifications are used by Eurostat. A sector corresponds to an economic activity defined at the NACE-4 code level, whereas a subsector corresponds to a product classified at the Prodcom 6- or 8-digit level. If a NACE sector is considered to be at risk of carbon leakage, all subsectors within this NACE category may benefit from the same carbon leakage status. Conversely, even if a sector as a whole is not at risk of carbon leakage, a subsector can still be assigned carbon leakage status and therefore be eligible for free allocation. Examples include Prodcom code 081221 ('Kaolin and other kaolinic clays'), and Prodcom code 10391725 ('Concentrated tomato puree and paste').

-

Sectors and subsectors exposed to a higher risk of carbon leakage

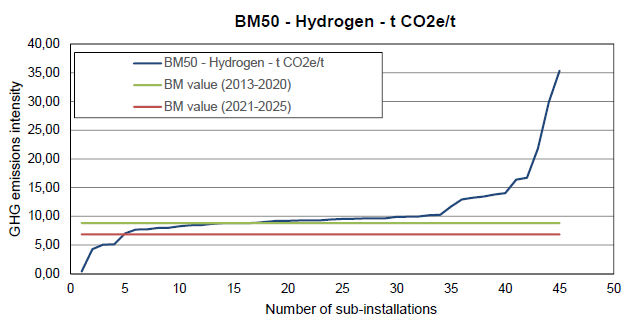

The sectors exposed to carbon leakage during the 2021-2030 period are those included in Commission Delegated Decision (EU) 2019/708 establishing the carbon leakage list (CLL), based on emissions and trade intensity indicators. These sectors are entitled to receive free allowances equal to 100 % of the relevant benchmark level. The benchmark level is based on the average GHG emissions intensity (in terms of CO2 equivalent emitted, per tonne of product produced or per terajoule) of the 10 % most efficient sub-installations covered by a given benchmark. All sub-installations producing benchmarked products are assigned to the corresponding product benchmark and depicted in a benchmark curve. Examples of product benchmarks include refinery products, ammonia, soda ash and hydrogen (see Figure 1 for the hydrogen benchmark curve).

Source: European Commission, Update of benchmark values for the years 2021-2025 of phase 4 of the EU ETS, 2021.

For each benchmark, only the 10 % most GHG-efficient sub-installations in a benchmark curve receive their full allocation free of charge, while the rest must purchase additional allowances to cover part of their emissions. The further a sub-installation is from the benchmark value representing the 10 % most efficient installations in terms of GHG emission intensity, the more allowances it will need to purchase to cover its emissions. In the example shown in Figure 1, only the five most efficient sub-installations covered by the hydrogen product benchmark in 2016-2017 would receive their full allocation free of charge during the 2021-2025 period, to comply with their emissions-related obligations.

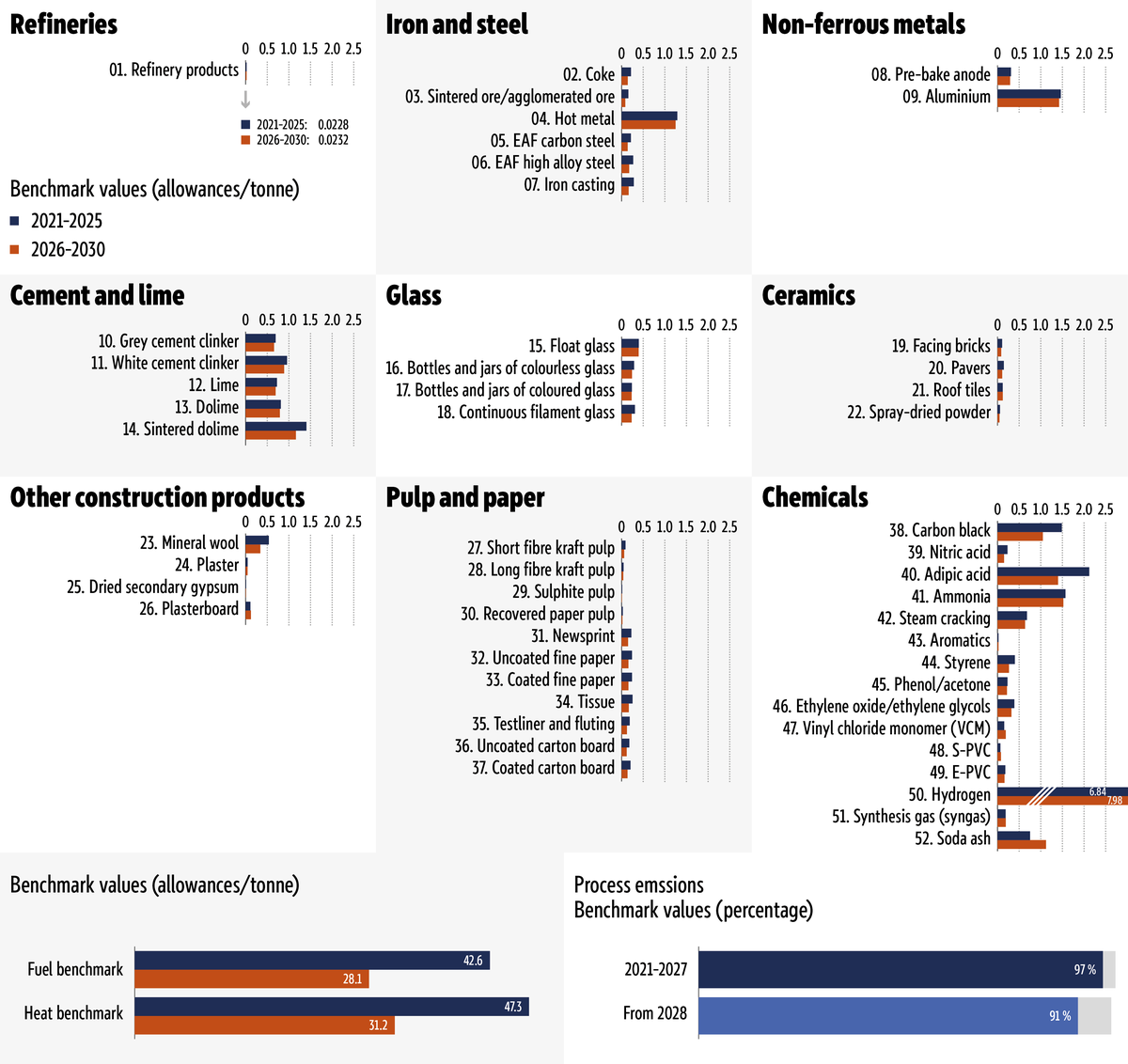

Through the benchmarking approach to free allocation, the EU ETS aims to reward sub-installations with the best average GHG emissions performance within each benchmark. The EU ETS covers 52 product benchmarks and two fallback benchmarks:

-

Product benchmarks (allowances per unit of product): These are output-based, calculated on the basis of the average GHG emissions of the best-performing 10 % of installations in the EU and the European economic area producing a specific product. For the 2021-2025 period, the benchmarks were based on the GHG emission intensities for 2016 and 2017, and for the 2026-2030 period, on the GHG emission intensities for 2021 and 2022.

-

Fall-back benchmarks (allowances per terajoule): These are input-based benchmarks (heat and fuel) for products and processes that cannot be covered by a specific product benchmark. These benchmarks are calculated on the basis of the amount of measurable heat or fuel consumed. Fall-back benchmarks apply across different sub-installations in all sectors where no product benchmarks are available or feasible. If neither a heat benchmark (the first fall-back option) nor a fuel benchmark (the second fall-back option) is feasible, a process emissions allocation approach applies.4

Regulation (EU) 2023/956 establishing the CBAM introduced a new category – 'CBAM sectors' – covering the goods listed in Annex I to the regulation. A first list of sectors with goods under CBAM include aluminium, hydrogen, fertilisers, iron and steel, and cement.5 Within this new category, a distinction is made between sectors and subsectors exposed to a high risk of carbon leakage that are covered by the CBAM and those that are not. For CBAM sectors, free allocation is gradually phased out through the application of a 'CBAM factor', which annually adjusts the level of free allocation in parallel with the gradual introduction (phase-in) of the CBAM.The CBAM factor will cease to apply from 2034, when free allocation for CBAM for these goods will end entirely.

This is not the case for non-CBAM sectors. While both CBAM and non-CBAM sectors are listed in the carbon leakage list (CLL), the CBAM factor does not apply to non-CBAM sectors. Furthermore, the amount of free allocation for non-CBAM sectors is determined for each product benchmark by the value set out in Commission Implementing Regulation (EU) 2021/447 setting the revised benchmark values for free allocation of emission allowances. The current benchmark values apply for the 2021-2025 period, and the Commission is required to update them for the 2026-2030 period.6 The Commission updated the benchmark list on 29 June 2026 (see Section on 'Updated benchmark values' below). For non-CBAM sectors, there is no announced free allocation phase-out deadline.7

What is carbon leakage?

Carbon leakage occurs when businesses have an incentive to transfer their activities and GHG emissions to other countries or jurisdictions with weaker carbon requirements. This situation can lead to an increase in global GHG emissions as long as businesses continue to emit somewhere else. GHG emissions shift to another location, potentially negating the benefits of the original climate policy. Traditionally, the EU has mitigated sectors' exposure to the risk of carbon leakage through the free allocation of emissions allowances. From 2026, a CBAM phases in a carbon price, equivalent to the EU ETS, on imports of certain goods, gradually replacing the free allocation system.

-

Sectors exposed to a lower risk of carbon leakage

Some sectors exposed to the risk of carbon leakage will continue to receive a reduced level of free allocation until 2030, after which free allocation will be fully eliminated. These are the sectors that are excluded from the carbon leakage list because they are considered to have a lower exposure to carbon leakage based on their emissions or trade intensity indicators.8 Examples of such sectors are 'mining of lignite', 'extraction of natural gas' and 'casting of light metals'. For sectors exposed to a lower risk of carbon leakage, free allocation is set at 30 % until 2026 and is to be gradually phased out by 2030. In addition, ETS installations providing heat to district heating systems may still continue receiving free allocation until 2030.

Certain Member States can also provide free allocation to electricity-generating installations to support investment in the modernisation of their energy sectors. Out of 10 eligible Member States, only Bulgaria, Hungary and Romania make use of this provision, which will end on 31 December 2030.

| Sector | Free allocation rate | Phase-out timeline | Phase-out date | Examples |

| Most exposed sectors (CBAM) | 100 % at the level of the percentile positioned in the 10 % most efficient sub-installations for each benchmark (the benchmark level) | An annual reduction rate ranging from 0.3 % to 2.5 %, multiplied by a 'CBAM factor'

(97.5 % in 2026, 95 % in 2027, 90 % in 2028, 77.5 % in 2029, 51.5 % in 2030, 39 % in 2031, 26.5 % in 2032 and 14 % in 2033) | 2034 | Iron and steel, aluminium, cement, fertilisers and hydrogen |

|---|---|---|---|---|

| Most exposed sectors

(non-CBAM) |

An annual reduction rate ranging from 0.3 % to 2.5 % | none | Refineries, chemicals, ceramics, glass, pulp and paper, etc. | |

| District heating | 30 % | 30 % rate remains until phase-out date | 2030 | |

| Less exposed sectors | 30 % | 30 % in 2025, 22.5 % in 2026, 15 % in 2028, 7.5 % in 2029 | 2030 | Sectors not in the CLL |

Data source: Compiled by the author on the basis of the legal provisions of the EU ETS Directive.

The concept of dynamic allocation was introduced in the EU ETS with the adoption of Commission Implementing Regulation (EU) 2019/1842 as regards adjustments to free allocation of emission allowances due to activity level changes. Dynamic allocation means that free allowances allocated to an installation receiving free allocation may be corrected later if its average activity level changes significantly, compared to a historical activity level initially used to determine its volume of free allocation.

A 15 % increase or decrease in production triggers the adjustment; this increase or decrease is determined by calculating a rolling two-year (arithmetic mean) average activity level for each sub-installation.9 Since 2021, dynamic allocation has replaced the older approach for the adjustment of free allocation volumes as a result of significant capacity changes. Dynamic allocation aims to better align free allocation with actual production volumes.

Conditionalities for free allocation

Conditionality refers to the requirements that eligible installations receiving free allocation have to meet in order to avoid a reduction in their level of free allocations. The concept of conditionality for free allocation was introduced in the 2023 revision of the EU ETS Directive and comprises three non-cumulative types:

-

conditionality related to energy efficiency improvement measures: Installations subject to an energy audit or a certified energy management system (under Article 8 of Directive (EU) 2023/1791 on energy efficiency) face a 20 % reduction in free allocation if they cannot demonstrate to their national competent authority that they have implemented the recommended energy efficiency measures.10

-

conditionality related to climate neutrality plans: Installations with product benchmarks can receive a 20 % reduction in free allocation if the GHG emissions of a specific sub-installation exceed the 80th percentile of the benchmark curve. The reduction in free allocation applies unless the installation has an approved climate neutrality plan. Commission Implementing Regulation (EU) 2023/2441 sets out the content and format of climate neutrality plans.

-

conditionality related to investments in district heating: 11 From 2026 to 2030, an additional 30 % free allocation for district heating installations is conditional on investments whose value is at least equivalent to the economic value of the additional free allocation. This additional free allocation is aimed at reducing GHG emissions before 2030 and achieving climate neutrality at installation or company level by 2050.

Updated benchmark values

Under Article 10a (2) of the EU ETS Directive, the European Commission is required to propose an updated list of benchmark values for the 2026-2030 period. The Commission had first planned the publication of the benchmark regulation for April 2026. However, the draft was sent for public consultation in May 2026, which lasted four weeks. It was then voted upon by Member States on 15 June in the Climate Change Committee. The vote was positive, with 17 Member States voting in favour, 5 against, and 5 abstaining. The updated benchmark values were then formally adopted and published in the EU Official Journal on 29 June. Industrial facilities will be required to surrender their emission allowances to the relevant authorities in September.

With the updated benchmark values, free allocation would decrease by more than 16 % on average in 2026 compared with 2021. While the heat and fuel fallback benchmarks would record some of the largest reductions (34 % each), other product benchmarks would increase.12 They would benefit from the inclusion of indirect GHG emissions from electricity use, alongside direct emissions, in the calculation of the average GHG emission intensities of the 10 % best-performing installations for each benchmark in 2021-202213.The new approach is expected to have a financial impact of around €4 billion more in free allocation.

Source: Compiled by the author on the basis of information extracted from Commission Implementing Regulation (EU) 2021/447 determining the benchmark values for 2021-2025, and Commission Implementing Regulation (EU) 2026/1412 determining the revised benchmark values the adopted for 2026-2030. Graphics by Samy Chahri, EPRS, 2026.

Revision of the EU ETS Directive

Following the adoption of Regulation (EU) 2026/667 as regards the setting of a Union intermediate climate target for 2040 and the adoption of amending Regulation (EU) 2021/1119 (the European Climate Law), the EU ETS is set to undergo a comprehensive and mandatory assessment. The Commission has announced that it would submit a proposal by July 2026. The EU target for a potential agreement between the European Parliament and the Council to revise the EU ETS Directive is Q1 2027.

In its proposal, the Commission will have to integrate the elements related to the EU ETS outlined in Recital 13 of the revised European Climate Law. As regards free allocation, the Commission should consider a slower phase-out pathway from 2028 onwards. In addition, the upcoming revision of the EU ETS Directive needs to address a number of issues, including the risk of carbon leakage in sectors not covered by the CBAM. The Commission's tender specifications regarding support for the review of the EU ETS and the market stability reserve, and the questionnaire released during the 2025 public consultation on the revision of the EU ETS Directive, offer clues about the Commission proposal's potential focus areas.

Among others, the Commission proposal could assess whether free allocation is an effective measure to achieve emissions reductions; whether the existing benchmark value system is the most effective approach; and whether free allocation would continue to offer protection against carbon leakage risk post-2030. The existing CLL, adopted in 2019, is only valid for the 2021-2030 period and would likely be updated ahead of 2030. Consequently, the Commission might assess whether different levels of exposure to carbon leakage in the CLL would increase the effectiveness of free allocation. The Commission impact assessment accompanying its proposal to revise the EU ETS Directive in 2021 already looked at the 'tiered approach', concentrating free allowances on sectors with the highest exposure to carbon leakage as a potential option for a more targeted approach to free allocation.14

In addition, the Commission may be considering introducing stricter conditionality requirements linked to investment supporting decarbonisation, among other options. The Commissioner for Climate, Net Zero and Clean Growth, Wopke Hoekstra, has confirmed that the upcoming revision of the EU ETS should condition free allocation on investment in the EU in support of decarbonisation objectives. This would add a further layer of conditionality to the existing requirements for granting free allocation to industry.

On 11 May 2026, when announcing the launch of the public consultation on revising the benchmark values for free allocation, the Commission stated that it will propose introducing sector-specific fallback benchmarks as part of the upcoming EU ETS revision. The revised methodology, if adopted in parallel to the revision of the EU ETS Directive, should be implemented as early as possible. On 19 June, the European Council conclusions on competitiveness and global challenges confirmed that the Commission will present a separate proposal alongside the revision of the EU ETS Directive.

Member States' and stakeholders' views

Already ahead of the draft publication of the updated benchmark values applicable for the 2026-2030 period, some Member States had been actively advocating for a relaxation of the current benchmark rules. In April 2026, the Czech Prime Minister called for additional free allocation, conditional on decarbonisation plans, for businesses in the most affected sectors and regions.Two days later, the Spanish Minister of Industry and Tourism sent a letter to the Commissioner for Climate, Net Zero and Clean Growth, expressing concerns about the update of the benchmark values and the lack of transparency. According to the minister, the update of the fuel and heat benchmark values should better reflect the diversity of industrial processes, for example, by introducing an unbundling mechanism with separate reference levels based on temperature ranges.15

The Italian Ministers of the Environment and Energy Security and of Enterprises and Made in Italy asked the European Commission to temporarily freeze the 2021-2025 benchmark values until the overall revision of the EU ETS Directive has taken place. Ahead of the Competitiveness Council of 28 May, Czechia, Greece, Poland and Romania made the same request. Later, government representatives from Estonia, France, Germany and Spain signed a non-paper expressing their concerns about the update of the heat and fuel fallback benchmarks. They called for a targeted legislative proposal to be adopted before January 2027, separate from the revision of the EU ETS Directive, and for retroactive application of the new benchmarks from January 2026. They argued that the proposed revision of the benchmark values could inadequately increase the carbon cost borne by industries in a context of extraordinary energy prices and global competition.

Along the same lines, in February 2026, energy-intensive industries submitted a letter asking for the suspension of further ETS benchmark reductions and the adoption of measures to avoid triggering the CSCF. They argued that, if triggered, the CSCF would further reduce free allocation for all sectors. In April, another letter, co-signed by energy-intensive companies, asked that, instead of tightening the fall-back benchmarks, they be kept at the 2021-2025 level or be subject only to the minimum annual benchmark reduction of 0.3 % for the same period, as defined in Article 10a of the EU ETS Directive. Business Europe has demanded, among other things, the extension of the carbon leakage list and the removal of the existing conditionalities for free allocation in the upcoming revision of the EU ETS Directive. On the other hand, NGOs such as Sandbag believe that increasing the volume of free allocation is not only unnecessary, but it would also undermine the EU's ability to reduce dependency on fossil fuels. Carbon Market Watch argues that free allocation continues to undermine investment incentives for zero-carbon solutions. Think tanks such as EPICO call for a more strategic approach to allocation while providing greater flexibility.

Further reading

- López Hernández, J.F, Revision of the EU emissions trading system, EPRS, European Parliament, January 2026.

- López Hernández, J.F., Update of the EU emissions trading system for stationary installations, aviation, and maritime transport, EPRS, European Parliament, April 2026.

Endnotes

Classification

Policy areas: Environment

Regions: European Union

Committees: Environment, Climate and Food Safety (ENVI)

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.