Article page checkbox is not checked in page info.

The implementation and impact of the VAT reverse charge mechanism in the EU: European implementation assessment

The implementation and impact of the VAT reverse charge mechanism in the EU

Mafalda Monda and Simona Megne, Ex-Post Evaluation Unit

Summary

To support the work of the European Parliament's Sub-Committee on Tax Matters on its non-legislative report on the implementation of the VAT reverse charge mechanism (2025/2261(INI)), the Ex-Post Evaluation Unit of EPRS produced a European implementation assessment on the implementation, effectiveness and future relevance of the VAT reverse charge mechanism in the EU. The study was conducted from February to May 2026 and covered all 27 EU Member States. In addition, Austria, Estonia, Italy, Spain, the Netherlands, Poland, Romania and Sweden were selected as case studies to provide more detailed insights.

The VAT reverse charge mechanisms

Value added tax (VAT) is one of the most important sources of public revenue in the EU. Under the EU VAT system, tax is collected at each stage of the supply chain, from production to final sale. Businesses charge VAT on their sales, deduct the VAT paid on their purchases and remit the difference to the tax authorities. However, VAT is particularly vulnerable to fraud, especially missing trader intra-Community (MTIC) fraud and carousel fraud schemes. In such schemes, a fraudulent trader supplies goods and services to other businesses, collects the tax due on the supply, and then disappears without remitting it to the tax authorities.

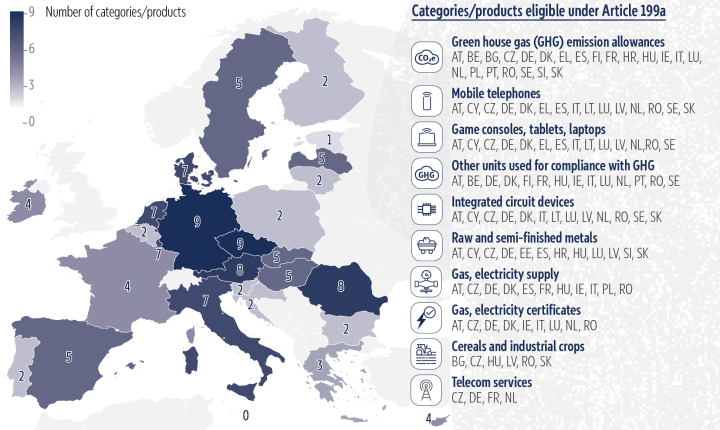

To address the fraud risks at EU level, two optional and temporary instruments were introduced: the reverse charge mechanism (RCM) and the quick reaction mechanism (QRM). The RCM, introduced under Article 199a of the VAT Directive, shifts the liability for payment of VAT from the supplier to the customer in transactions occurring in predefined sectors/product categories (see Figure 1), thus reducing the risk of VAT fraud caused by MTIC schemes. The QRM, under Article 199b of the VAT Directive, allows Member States to apply the RCM in situations of sudden and massive fraud, regardless of sector, providing a flexible and rapid response to emerging fraud threats. Both instruments are currently operational until end-2026.

Source: 'The implementation and impact of the VAT reverse charge mechanism in the EU', CEPS and Ecorys, 2026; graphic by Nadejda Kresnichka-Nikolchova, EPRS.

The EU implementation map (see Figure 1) shows that, while most Member States currently apply the RCM to at least one sector, the breadth of its use varies substantially. Some countries apply it only in one narrowly defined category/sector, while others use it across a broader range of sectors. The most common current category concerns transfer of emissions allowances, applied in 22 Member States. The least applied categories concern cereals and industrial crops, applied in six Member States, and telecom services, applied in four Member States.

European implementation assessment: Key findings

This European implementation assessment, composed of an introduction by EPRS and an external study drawn up by the consortium of CEPS and Ecorys, examines the use of RCM and QRM by Member States, its effectiveness in reducing VAT fraud, the impact on businesses and tax administrations, and whether there is a need to extend or revise both mechanisms beyond their current expiry date. The European implementation assessment also aims to support the decision-making process regarding the future use of the RCM and QRM.

The study identifies the following key findings:

RCM

-

The RCM under Article 199a of the VAT Directive remains relevant as a targeted anti-fraud instrument, particularly in sectors vulnerable to MTIC and carousel fraud, such as electronics, emissions-related trading, energy-related markets, and metals and other commodities.

-

Evidence collected for the study indicates that the mechanism has contributed to reducing fraud risks in these sectors and is generally viewed by the tax authorities as an effective tool in the fight against VAT fraud.

-

The effectiveness of the mechanism depends on clear legal rules, workable implementation, administrative capacity and effective monitoring.

-

Use of the RCM can reduce fraud opportunities, but it may also shift fraud towards other sectors, products or Member States.

-

There are differences in implementation, as well as variations in definitions of sector, thresholds and administrative procedures across the EU.

-

All of these aspects may also create compliance costs and legal uncertainty for businesses.

QRM

-

The QRM under Article 199b of the VAT Directive has never been activated since its introduction.

-

Nevertheless, the study found that the mechanism remains relevant, particularly when Member States need to respond quickly to sudden and large-scale VAT fraud that falls outside the scope of Article 199a.

-

The mechanism is generally considered difficult to use in practice, as tax authorities may struggle to gather the necessary evidence and complete the required procedures quickly enough to respond to sudden risks of fraud.

Lessons learnt and recommendations

The external study recommends that the post-2026 policy choice should be framed as continuity with targeted reform of both mechanisms rather than simple extension or expiry.

The RCM should remain available beyond 2026 as a targeted anti-fraud measure, particularly during the transition towards the VAT in the Digital Age (ViDA) framework and wider digital VAT controls. However, its continued use should be subject to regular review, demonstrated fraud risk and proportionality.

The QRM should only be prolonged if it is made more practical and operationally usable, allowing Member States to respond more effectively to sudden fraud and large-scale fraud risks.

Together, these measures should form part of a broader and increasingly digital EU VAT anti-fraud framework.

Full study

Read the full study in pdf format, on the Think Tank website.

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.