Article page checkbox is not checked in page info.

Targeting VAT fraud: Role of the reverse charge mechanism

Targeting VAT fraud: Role of the reverse charge mechanism

Pieter Baert, Members' Research Service

Summary

Value added tax (VAT) is a cornerstone of national public finances and an important source of revenue for the EU budget. Missing trader intra-Community (MTIC) fraud – often perpetrated by organised criminal networks – is among the most damaging forms of VAT fraud, causing annual revenue losses running into the billions, and underscoring the need for effective anti-fraud tools.

One such tool is the reverse charge mechanism, under which the liability to account for VAT is shifted from the supplier to the customer.

The EU VAT Directive's optional reverse charge mechanisms – Articles 199a and 199b, introduced in 2010 and 2013 respectively – are currently authorised until 31 December 2026. Given their exceptional and time-limited nature, it would appear timely to assess how these mechanisms operate in practice, and how effective they have been in addressing MTIC fraud, with a view to their possible extension.

Introduction

Value added tax (VAT) is a cornerstone of each EU Member State's tax system. Each year, more than €1.2 trillion in VAT revenue is raised across the EU, accounting for roughly a fifth of all tax revenue collected (including social contributions). Since the 1970s, VAT has also been one of the EU's own resources (16 % of the EU budget in 2024).

Given its critical budgetary role, persistent losses of VAT revenue due to fraud are a major concern. While precise figures for the amounts lost due to VAT fraud are, by definition, challenging to determine, estimates suggest it runs tens of billions of each year in Europe. At a time when many Member States face tight public finances and growing expenditure pressures – particularly in areas such as defence – combating VAT fraud remains a pressing priority at both the national and EU level. In recent years, the EU has adopted a range of administrative and legislative measures to address VAT fraud, including enhanced information exchange between tax authorities (such as Eurofisc's transaction network analysis tool), detailed reporting requirements for businesses (VAT in the Digital Age package), and adaptions to the VAT rules to close possible loopholes for fraudsters, such as the reverse charge mechanism.

Against this backdrop, Articles 199a and 199b of the EU VAT Directive (Council Directive 2006/112/EC) establish optional reverse charge mechanisms to counter VAT fraud, the application of which is currently authorised until 31 December 2026.

VAT core principles

As a broad-based consumption tax, VAT is built on several fundamental principles, laid down in the VAT Directive, that underpin its operation across the EU.

First, unlike a single-stage sales tax, VAT is levied at each step of the production and distribution chain, from initial production through to final sale. At each stage, the tax is collected through a system of fractional payments, whereby each business remits only the VAT corresponding to the value added at that stage of the supply chain.1

Second, while VAT is applied at each stage in the supply chain, the ultimate economic burden falls exclusively on the final consumer, i.e. private consumption. Businesses charge VAT on their sales ('output VAT') and remit it to the tax authorities, while paying VAT on their purchases ('input VAT'), which they are generally entitled to deduct from the VAT charged on their sales.2 As a result, businesses do not bear the direct financial cost of VAT themselves; only private consumers do.3

Third, VAT liability rests with the supplier (Article 193 of the VAT Directive). As a general rule, the supplier, and not the customer, is required to charge, collect and remit the VAT to the tax authorities, regardless of whether the supplier is established in the Member State where the tax is due. This reflects the practical reality that the supplier controls the transaction, issues the invoice and receives the payment.

The VAT Directive nevertheless provides for limited exceptions where the liability to pay the VAT switches from the supplier to the customer, including under Articles 199a and 199b.4 As derogations from the general rule, these mechanisms are narrowly defined and apply only in specific circumstances.

Missing trader intra-Community fraud

While VAT fraudsters may employ multiple schemes, each varying in complexity, their goal is generally the same: either to inflate the input VAT claims artificially (to receive undue refunds) or to under-report – or fail to report – the output VAT (to retain the funds illegally). Such fraud generates substantial revenue losses for public finances, potentially forcing Member States to raise other taxes to compensate for the shortfall, and distorts the level playing field for compliant businesses.5

Among the different types of VAT fraud, missing trader intra-Community fraud (MTIC fraud) stands out as the most damaging. Recent estimates suggest that annual MTIC fraud-related losses in the EU range from €12.5 billion to €32.8 billion (1 % to 3 % of total VAT revenue).

Intra-Community supplies

Intra-Community supplies, and how they are treated for VAT purposes, are key to understanding how MTIC fraud works.6

In short, intra-Community supplies are those where a business supplies goods to another business (B2B), with the goods physically transported from one EU Member State to another.7 For VAT purposes, two distinct transactions occur: a tax-exempt intra-Community supply by the seller and – as its mirror image – a taxable intra-Community acquisition by the customer.

-

Tax exempt intra-Community supply in the Member State where the goods transport begins ('Member State of departure'):8 the supplier issues an invoice, including both their own VAT number 9 and that of the customer, and specifies that the supply is VAT exempt because of its qualification as an intra-Community supply.

-

Taxable intra-Community acquisition in the Member State where the goods finally arrive ('Member State of destination'):10 the business customer self-accounts for the VAT on the intra-Community sale of goods. Although the customer is liable for the VAT due on the acquisition, no actual payment is made, as the VAT is deducted simultaneously as input VAT.

Although the two-step treatment of a single intra-Community sale may initially appear complex or counterintuitive, it offers clear advantages for both suppliers and customers. For the supplier, the exempt supply in the Member State of departure removes the need to register for VAT in the Member State of destination, a process that would entail time, cost and compliance with foreign VAT rules, such as local rates and payment deadlines. The customer benefits, as well, as VAT on the intra-Community acquisition is self-accounted for and can be deducted in the same VAT return, thereby avoiding any upfront cash-flow impact.

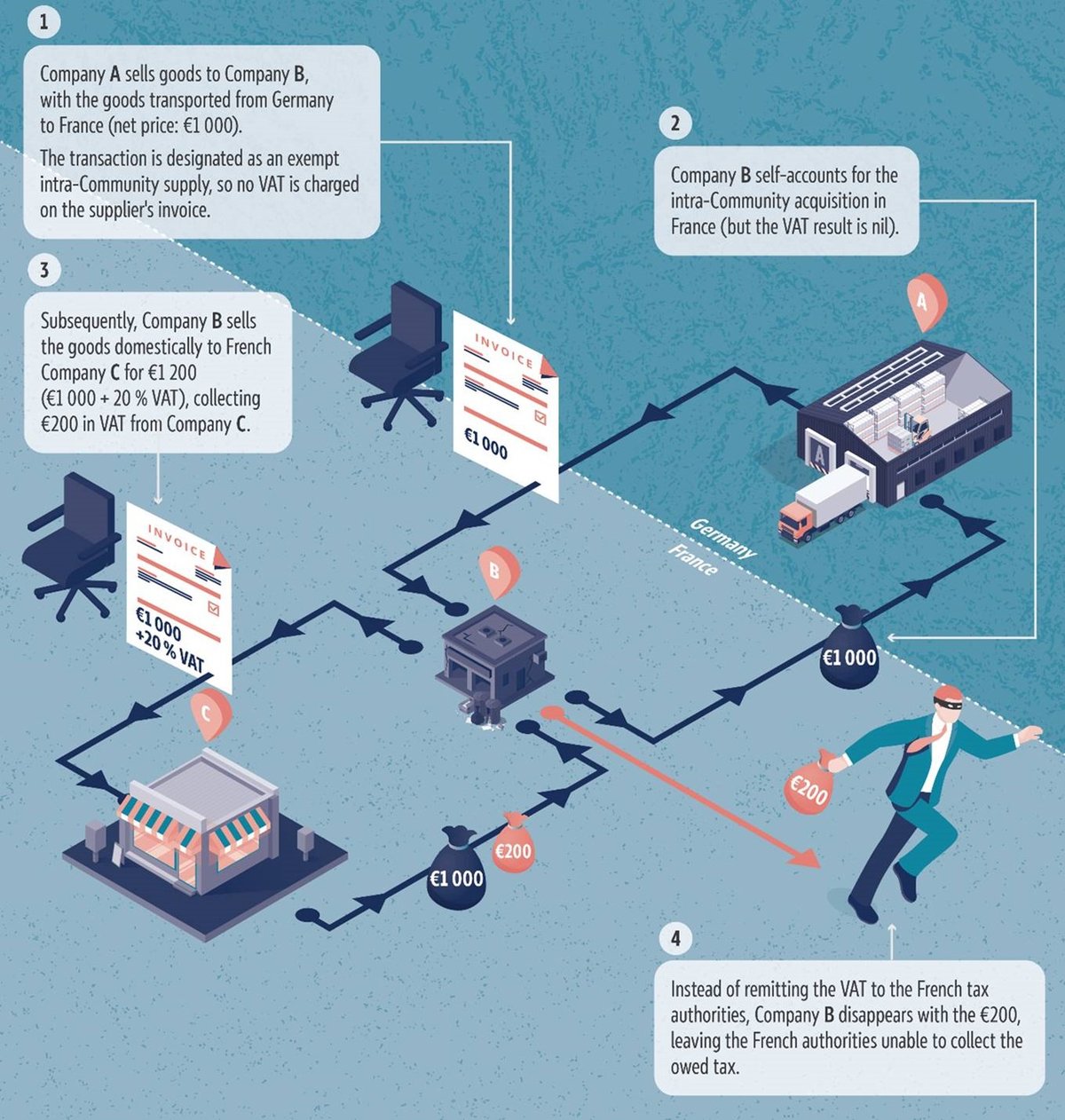

Missing trader

While administratively simple, the system creates a 'break' in the VAT payment chain, as no VAT is actually collected on the intra-Community supply. MTIC fraud exploits this gap: goods are purchased VAT-free from another Member State, VAT is then charged on onward domestic sales, and the trader subsequently disappears without remitting the tax (hence 'missing trader'; see Figure 1 for a basic example).11

Source: P. Baert, Filling the gap: The EU's fight against VAT fraud, EPRS, European Parliament, 2025. Graphic by Lucille Killmayer and Györgyi Mácsai, EPRS

While the example above is straightforward, detecting and prosecuting MTIC fraud is highly complex. Fraudsters may intermingle fraudulent transactions with legitimate ones to evade detection by authorities. The complexity is further exacerbated by 'buffer companies' in the transaction network. These companies (sometimes located in different Member States) serve to lengthen and obscure the VAT chain, making the fraud more difficult for the authorities to detect and trace. Buffer companies may also be operated by honest, tax-compliant businesses who unknowingly become entangled in a fraudulent chain, making judicial proceedings more difficult, as authorities try to distinguish between those deliberately participating in the fraud and those inadvertently caught up in it.12 The fraudsters use high-value items that are easy to move, such as mobile phones and laptops, in order to save on logistical and transportation costs.

Missing traders stay under the radar: they may operate under false names, or under the VAT registration number of a legitimate business without the rightful owner's knowledge. Transaction data are falsified or omitted from reporting. By the time the authorities have detected irregular data – for instance, sudden increases in the number of transactions, or imbalances in VAT statistics – in the (aggregated and monthly/quarterly) data from recapitulative statements, Intrastat reports or VAT returns, the fraudsters have already vanished.

A more extreme, extended version of MTIC fraud is carousel fraud.13 As the name implies, this scheme operates similar to a carousel: the same goods are bought and (re)sold in a circular pattern, ultimately returning to the original supplier (A->B->C->A->B->C->A-> ...). Once the goods complete a cycle, the process starts again, this time perhaps involving a new set of companies, but controlled by the same fraud network. With each cycle, fraudsters exploit the VAT system, increasing the fraudulent proceeds for the soon-to-be-missing traders.14

Owing to the complex, cross-border nature of MTIC fraud, the culprits are regularly part of organised criminal networks, with the proceeds transferred offshore and used to finance illegal activities. VAT fraudsters have been linked to money-laundering, drugs and even terrorism.15 In 2015, the European Court of Auditors estimated that 2 % of organised crime could be behind 80 % of MTIC fraud cases, highlighting that the issue extends beyond fiscal revenue and has wider implications for economic and internal security.

Reverse charge mechanism

One way to stop MTIC fraud is what is known as the reverse charge mechanism.

Under the normal VAT rules for domestic transactions, the supplier charges VAT and remits it to the tax authorities. Under the reverse charge, this obligation is reversed: the liability to account for VAT shifts from the supplier to the customer, who must calculate the VAT due on the supply and report it in its VAT return (hence 'reverse charge').16 The mechanism's logic is straightforward: by shifting the liability from the supplier to the customer, the supplier is prevented from receiving VAT and not remitting it to the tax authorities. By its nature, the reverse charge can only apply to B2B transactions, as only businesses can self-account for VAT.17

Sector-based reverse charge provision (Article 199a)

Member States seeking to apply the reverse charge to counter MTIC fraud had to rely on Article 395 of the VAT Directive, which allows derogations from the standard VAT rules to combat fraud.18 This procedure was widely considered lengthy and cumbersome, as it can take up to eight months for the Commission to table a proposal, and requires unanimous Council approval.

Against this backdrop, and in the wake of a series of high-profile VAT fraud scandals causing revenue losses of billions of euros across several Member States – most notably in relation to carbon credits trade19 – the Commission tabled a proposal in 2009 to allow Member States to apply the reverse charge in certain sectors. The Council adopted the proposal in 2010.

Initially limited to the trade in greenhouse gas emission allowances, Article 199a was subsequently extended to other sectors considered particularly vulnerable to VAT fraud, including mobile phones, tablets and laptops (see Table 1). These sectors are characterised by high value, high liquidity and ease of cross-border trading, facilitating rapid circulation through trading chains.

From the outset, this mechanism was conceived as temporary, initially applicable until 30 June 2015. However, its application has been repeatedly extended, first to 31 December 2018, then to 30 June 2022 and currently to 31 December 2026.

| Article 199a | Transactions |

|---|---|

| (a) | Transfer of allowances to emit greenhouse gases as defined in Article 3 of Directive 2003/87/EC establishing a scheme for greenhouse gas emission allowance trading |

| (b) | Transfer of other units that may be used by operators for compliance with the same directive |

| (c) | Supplies of mobile telephones |

| (d) | Supplies of integrated circuit devices |

| (e) | Supplies of gas and electricity |

| (f) | Supplies of gas and electricity certificates |

| (g) | Supplies of telecommunication services |

| (h) | Supplies of game consoles, tablet PCs and laptops |

| (i) | Supplies of cereals and industrial crops |

| (j) | Supplies of raw and semi-finished metals |

Data source: VAT Directive.

Some subcategories or specific details were omitted from the overview for ease of reading. The application of the reverse charge to the supply of any of the goods or services listed in points (c) to (j) is subject to the introduction of appropriate and effective reporting obligations on businesses who supply the goods or services.

Quick reaction mechanism (Article 199b)

On a proposal from the Commission designed to respond more swiftly to the rapidly evolving nature of VAT fraud, a quick reaction mechanism (QRM) was introduced in 2013. As a fall-back option to Article 199a, this mechanism allows Member States, in cases of 'sudden and massive fraud', to temporarily apply the reverse charge without being limited to predefined transactions.

However, this comes under strict conditions: if a Member State wishes to introduce the QRM, it needs to notify the Commission and the other Member States, providing information about the sector concerned, the type and features of the fraud, why the situation is urgent, why the fraud is sudden and massive, and the expected financial losses. Once the Commission has all the necessary information, it has one month to object or confirm the use of the QRM. The Member State may then immediately apply the QRM from the date of confirmation for a maximum of nine months. The QRM thus acts as a bridging measure allowing Member States to respond rapidly to sudden and massive fraud while the standard derogation procedure under Article 395 is being completed.

Similar to Article 199a, the QRM was put in place as a temporary measure, initially applicable until 31 December 2018. However, its application has been repeatedly extended, first to 30 June 2022 and currently to 31 December 2026. No Member State has so far applied the QRM.

| Sector-based reverse charge | Quick reaction mechanism | |

|---|---|---|

| Article | 199a | 199b |

| Application | Temporary (until 31 December 2026) | Temporary (until 31 December 2026) |

| Optionality | Optional | Optional |

| Scope | Dedicated list of sectors | Not specified |

| Conditions | Member State is faced with sudden and massive fraud liable to lead to considerable and irreparable financial losses |

Data source: Compiled by the author.

Generalised reverse charge mechanism

Between 2019 and 2022, the VAT Directive temporarily provided for a generalised reverse charge mechanism (GRCM) under Article 199c. This mechanism allowed Member States, under strict conditions, to apply the reverse charge to all domestic supplies of goods and services exceeding €17 500 per transaction. Eligibility was limited to Member States where at least 25 % of the national VAT gap was attributable to carousel fraud. Ultimately, no Member State made use of this measure.

Effectiveness and risks

The introduction of the reverse charge may also entail some administrative costs and risks. If applicable, businesses may need to install and operate parallel accounting processes for transactions subject to the reverse charge and those subject to the normal VAT rules. Errors are also possible where suppliers apply the normal VAT rules instead of the reverse charge, leading to corrective actions for both parties. A 2014 study made for the European Commission also indicated stakeholders' concern about the lack of a uniform classification of the goods and services subject to the reverse charge, leading to differences in interpretation.

On a broader level, concern exists about a potential 'domino effect', whereby fraudsters shift their activities either to sectors not covered by the reverse charge or to other Member States where the mechanism does not apply. Additionally, the reverse charge departs from the traditional VAT system of fractional payments: rather than VAT collected at each stage of the supply chain, it is pushed towards the very last step, usually the retail sector. This, in turn, concentrates fraud risks at the end of the chain, creating what is referred to as the 'last-mile problem'.20

In 2018, the Commission issued a report on the application and effects of Articles 199a and 199b. The report showed that Article 199a had been widely used by Member States, particularly in relation to greenhouse gas emission allowances and mobile phone trade. Overall, Member States viewed the sector-based reverse charge under Article 199a as an effective tool to counter MTIC fraud. Several reported higher VAT revenues and a sizeable reduction – sometimes even the disappearance – of fraud in the sectors concerned. The mechanism was also seen as contributing to a more level playing field for compliant businesses. While estimates of the scale of VAT fraud – or of fraud effectively averted – are inherently difficult to quantify, available empirical evidence from academic research suggests that the reverse charge has had a positive impact in reducing MTIC fraud in the sectors where it is applied.21

According to the Commission's report, business stakeholders similarly acknowledged the usefulness of Article 199a in addressing VAT fraud. Without it, compliant businesses may otherwise become inadvertently involved in MTIC fraud chains, facing denied VAT deductions, legal costs and lengthy audits, and often requiring substantial investment in enhanced due-diligence checks on trading partners. The reverse charge mechanism eliminates this risk.

Views on the QRM (Article 199b) were more mixed. While its objective of enabling a rapid response to sudden and massive fraud was broadly supported, several Member States questioned the QRM's practical utility, considering the eligibility criteria as overly strict and difficult to meet in practice. So far, no Member State has made use of the QRM.

Future of the reverse charge

The reverse charge mechanism remains an exception to the general VAT rules. An extension beyond 2026 requires careful assessment, weighing both benefits and drawbacks. At the same time, the question arises of whether other tools could replace or complement the reverse charge.

Origin and destination

The most far-reaching response to MTIC fraud would be to remove the VAT exemption for intra-Community supplies of goods altogether, and to subject such transactions to taxation, thereby closing the systemic vulnerability. In the 1990s and early 2000s, the EU explored a VAT system based on the origin principle, under which goods would be taxed in the Member State where transport begins. To prevent distortions of competition and the relocation of suppliers to low-VAT jurisdictions, such a system would have required a high degree of VAT rate harmonisation across Member States. As there was limited political will to do this, the origin-based system was ultimately abandoned.

In 2017, the Commission put forward a new proposal for reform, based on the destination principle, known as the 'definitive system'. Under this model, VAT on cross-border supplies would be charged by the supplier at the rate applicable in the Member State of destination, while being initially collected by the tax authority of the Member State of origin and subsequently transferred to the customer's Member State. The proposal failed to secure sufficient Council support and was withdrawn in 2025.22

Digital tools

In recent years, Member States have increasingly relied on digital tools to strengthen VAT enforcement. Many are implementing digital VAT reporting requirements (DRRs), requiring businesses to exchange a detailed track of their sales and purchases with the tax authorities in near-real time. This fast, automatic and digital exchange of information – about the seller, the customer, the VAT charged and the individual transactions while they are taking place – allows the tax authorities to keep a close eye on transactions and the related VAT trail, and to intervene when they believe that there is fraud at hand. Evidence suggests that DRRs have already contributed to a reduction in VAT fraud, with estimates indicating that DRRs generated an additional €19 billion to €28 billion in VAT revenue in the EU between 2014 and 2019. Looking ahead, Member States are expected to expand national DRRs further, particularly following the adoption of the VAT in the Digital Age package, contributing to the fight against MTIC fraud.

Cooperation

Given the cross-border nature of MTIC fraud, the EU has emphasised administrative and judicial cooperation between Member States. Bodies such as Eurofisc (a network of liaison officials from the 27 Member States and Norway, launched to combat cross-border VAT fraud), Europol, Eurojust (the EU Agency for Criminal Justice Cooperation), OLAF (the EU Aanti-Fraud Office), and, more recently, the European Public Prosecutor's Office (EPPO), each operating within distinct mandates covering risk analysis, information exchange, criminal investigation, and prosecution.

In November 2025, the Commission tabled a proposal to strengthen the cooperation of Eurofisc, EPPO and OLAF to combat VAT fraud, in light of a wider review of the EU's anti-fraud architecture. The Commission considers that the current information exchange is incomplete and slow, reducing the effectiveness of efforts to combat VAT fraud. To address these shortcomings, the Commission proposes to provide to the EPPO and OLAF a more direct and streamlined communication with Eurofisc and a specific, direct and centralised access to relevant VAT information.

European Parliament position

The European Parliament has consistently emphasised the need to strengthen the fight against VAT fraud.

While the latest extension of Articles 199a and 199b received broad political support, Parliament requested that the Commission assess the effects of the reverse charge mechanism before any further extension.23

Endnotes

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.