Article page checkbox is not checked in page info.

The interim evaluation of the European Defence Fund

The interim evaluation of the European Defence Fund

Sebastian Clapp, Members' Research Service

Summary

The European Defence Fund (EDF), launched in 2021, has become a central instrument in promoting joint defence research and capability development, defence innovation and cross-border industrial cooperation. Over 160 collaborative projects have been launched within the framework of the EDF, in which over 1 300 entities across 26 Member States (all except Malta) as well as Norway participate.

The June 2025 interim evaluation confirms that the Fund has helped reduce duplication, enhanced SME participation, and stimulated pan-European cooperation, but warns that, without procedural simplification, stable co-financing and closer integration with national planning, its long-term potential risks being undercut. The Commission has also called for a substantial EDF funding increase in the 2028-2034 multiannual financial framework.

The European Parliament underscores the EDF's vital contribution to capability development, innovation and technological sovereignty. It consistently calls for increased funding, stronger parliamentary oversight and closer alignment with instruments such as permanent structured cooperation (PESCO) and the coordinated annual review on defence (CARD). Parliament stresses the need for faster, more flexible procedures and insists that EDF-supported projects must reflect jointly defined military priorities to deliver real strategic impact.

Introduction

The EDF, launched in 2021 under the current multiannual financial framework (MFF), marked a notable institutional step in the EU's evolving approach to defence capability development. The €8 billion fund incentivises cross-border cooperation in defence research (for which €2.7 billion is budgeted) and development (for which €5.3 billion is budgeted). The EDF received a €1.5 billion increase through the mid-term review of the MFF, but rather than being used for additional projects under the EDF, these funds were earmarked for the future European defence industry programme (EDIP), which is still under negotiation.

The EDF builds on two earlier programmes: the €500 million European defence industrial development programme (EDIDP) and the €90 million Preparatory Action on Defence Research (PADR). It aims to address longstanding structural issues in the European defence technological and industrial base (EDTIB), including fragmentation, duplication and insufficient investment coordination among Member States (see below). The Fund can cover up to 100 % of the total eligible costs of selected projects, primarily through grants, which may also include bonuses of up to 35 %. Research activities are eligible for full funding, whereas capability development activities are subject to varying co-financing rates designed to complement national or industrial contributions, ranging from 20 % to 80 % depending on the stage, from prototyping to certification. Additional incentives are available through a bonus system that rewards the participation of small and medium-sized enterprises (SMEs), mid-caps, and links to permanent structured cooperation (PESCO) projects.

The Commission's interim evaluation of the EDF, published in June 2025, provides an opportunity to examine the Fund's early implementation. While the EDF is still at a formative stage (no completed projects at the time of evaluation) the report offers insights into the EDF's performance, participation patterns and emerging outcomes.

| Company | Country | Revenue in US$ million | Global ranking |

|---|---|---|---|

| Airbus | European | 12 900 | #13 |

| Leonardo | Italy | 12 401 | #14 |

| Thales | France | 10 593 | #17 |

| Rheinmetall | Germany | 6 145 | #20 |

| Naval Group | France | 4 604 | #27 |

| Saab | Sweden | 4 377 | #29 |

Source: Defense Top 100, 2024.

Strategic context

The EDTIB is composed of a diverse range of actors, including major prime contractors, mid-caps and a substantial number of SMEs. In 2022, the Commission estimated the sector's annual turnover to be roughly €70 billion, with direct employment for around 500 000 people. Industrial capacity is largely concentrated in a few EU Member States, notably France, Germany, Italy, Spain and Sweden. Nevertheless, analysis by the Defence Joint Procurement Task Force that brings together the European External Action Service (EEAS) with the EU Military Staff, the European Defence Agency (EDA) and the Commission, indicates a wider geographic spread than top-level figures suggest: 46 of the most urgent defence capabilities are produced in 23 different Member States.

The EDTIB suffers from two persistent structural issues: chronic under-investment and deep fragmentation in both demand and supply. Despite longstanding commitments by EU and NATO member states – most notably NATO's 2 % of GDP spending target from 2014 and PESCO pledges from 2017 to increase defence budgets in real terms – investment has remained well below expectations prior to 2025 (before NATO's new 5 % commitment and the €800 billion being leveraged under Rearm Europe/Readiness 2030). According to the Commission, had all EU Member States met the 2 % target between 2006 and 2020, an additional €1.1 trillion would have been available for defence. Defence budgets that were available were not consistently directed toward the EDTIB, even where suitable EU products existed. Between 2007 and 2016, more than 60 % of European defence procurement was spent outside the EU. Following Russia's 2022 invasion of Ukraine and increased European defence purchases, this dependency deepened, with 78 % of defence acquisitions from February 2022 to June 2023 sourced from abroad, and 63 % from the United States alone.

The fragmentation of Europe's defence sector compounds the problem. On the demand side, only 18 % of investments and procurements are collaborative, according to data from 2021. National priorities dominate procurement decisions, favouring domestic industry and resulting in a proliferation of small, nationally focused defence firms. This weakens Europe's collective capacity to scale production or respond strategically to current threats. As the Strategic Compass acknowledges, European initiatives will remain limited unless national defence planning becomes more aligned with EU efforts. Greater collaboration, according to EPRS estimates, could generate savings from €18 billion to €57 billion annually.

Supply-side fragmentation is equally detrimental. The EDTIB remains structured along national lines, particularly outside the missile and aerospace sectors. The Commission has highlighted that this undermines competitiveness by preventing pooled R&D and scaled production, resulting in duplication, logistical inefficiency and poor interoperability. A striking example is the development of sixth-generation fighter aircraft: instead of pooling resources into a single programme, two separate projects are underway. One, the Future Combat Air System (FCAS), involves France, Germany and Spain, while a second, the Global Combat Air Programme, was launched by Italy and the United Kingdom, later joined by Japan.

The EDF tackles both under-investment and fragmentation by funding joint projects that require cross-border cooperation. It incentivises collaborative procurement and shared R&D, helping Member States pool resources, reduce duplication and strengthen the EDTIB. In doing so, it operationalises key goals of PESCO and the Strategic Compass, making EU defence more integrated and efficient. The Strategic Compass for Security and Defence, approved in March 2022, sets out a renewed agenda for enhancing the EU's security and defence posture. At its core lies a commitment by Member States to increase defence expenditure substantially and improve the efficiency of spending by enhancing interoperability, reducing fragmentation and leveraging key EU instruments, most notably the EDF and PESCO. The Compass frames these mechanisms as essential to strengthening the EDTIB and supporting collaborative defence research, capability development, and innovation. The EDF is presented in the Strategic Compass as a central enabler of defence cooperation; it is described as instrumental in fostering collaborative projects that address capability shortfalls, promote interoperability, and counteract the persistent fragmentation of Europe's defence landscape. The Compass underscores the need for Member States to make full and coherent use of the Fund, aligning national investment efforts with EU-level tools to maximise strategic effect and reinforce collective readiness. The EDF is also recognised for its role in boosting the competitiveness and resilience of the EDTIB, and the Compass calls for enhanced synergies with other defence initiatives to ensure policy coherence and operational impact.

This strategic orientation was further advanced with the Commission's adoption of the first-ever European defence industrial strategy (EDIS) on 5 March 2024. EDIS sets out a vision for unlocking the full potential of the EDTIB. It identifies structural gaps and proposes a roadmap for improving industrial responsiveness and investment coherence. At the heart of the strategy is the call for Member States to 'invest more, better, together and European', a formula intended to translate political commitment into meaningful industrial capability. EDIS also proposes the EDIP as a new framework to accelerate progress, while reaffirming the importance of existing instruments such as PESCO and the EDF. Within this framework, the EDF emerges as a cornerstone instrument for reinforcing the EDTIB. It has enabled significant progress in cross-border cooperation, innovation, and the reduction of industrial fragmentation. The Fund's success is exemplified by its engagement of over 400 entities across 26 Member States (all except Malta) and Norway, its targeted support for SMEs, and its alignment with PESCO priorities. However, both the Strategic Compass and EDIS acknowledge that the EDF's current financial allocation is insufficient to match the scale of Europe's strategic ambition. The Commission therefore calls for a substantial, predictable and sustained increase in funding within the next MFF to consolidate gains and ensure long-term industrial resilience.

Complementarity between the EDF and PESCO?

PESCO and the EDF are complementary tools to strengthen EU defence cooperation. PESCO provides a legal framework for Member States to jointly develop military capabilities, while the EDF offers EU funding for collaborative defence projects. To encourage alignment, the EDF grants a 10 % co-financing bonus to eligible development activities undertaken as part of a PESCO project. This financial incentive aims to translate political commitments into concrete industrial outcomes. To date, 53 EDF projects have been undertaken as part of a PESCO project (33 % of projects). As an example, the EU HYDEF EDF project, which aims to develop a European endo-atmospheric interceptor capable of countering threats expected beyond 2035, is linked to the PESCO project TWISTER.

According to experts, the most effective scenario for EU defence integration would maximise the objectives of both the EDF and PESCO by enabling the joint development of key capabilities identified at EU level. However, achieving this requires reforms: a realistic and embedded capability planning process, stricter project selection by the PESCO Secretariat, and an improved, top-down CDP-CARD framework on the capability development process. Without such alignment, various suboptimal scenarios risk inefficiency, fragmentation and political tension.

This direction is further endorsed in the March 2025 White Paper for European Defence – Readiness 2030, which reiterates the centrality of the EDF to fostering cross-border cooperation, reducing industrial fragmentation, and supporting collaborative capability development. The White Paper stresses the need for closer alignment between the EDF and national defence budgets to improve coherence in planning and investment. It strongly recommends reinforcing the EDF in the next financial cycle, arguing that the evolving security environment necessitates a significantly larger and more strategically embedded instrument to enhance European readiness and resilience. The White Paper also notes key capability gaps already recognised by Member States in EU and NATO planning and urges joint action to address them through Defence Projects of Common European Interest, supported by EU incentives. This cooperation would help Member States meet NATO targets more efficiently and with greater interoperability. It also outlines steps to strengthen the European defence industrial base, boost research, and build a unified defence equipment market.

Simplification of EDF procedures

The Commission put forward the Defence Readiness Omnibus in June 2025. In the interim evaluation of the EDF, the Commission identifies the need to streamline procedures and reduce bureaucracy in the EDF. In response, the Commission proposes a range of simplifications, including more flexible award criteria, expanded options for indirect management and clearer rules for direct awards. These changes aim to accelerate project implementation and enhance predictability. Additional measures include higher subcontracting thresholds, extended validity of ownership assessments, and a standard non re-transfer clause. Existing EDF projects may be simplified retroactively. Furthermore, to enhance cooperation with Ukraine, testing activities conducted there will become eligible for EDF funding, enabling rapid integration of battlefield feedback into European defence innovation, in line with the objectives of the Strategic Technologies for Europe Platform.

According to the Commission, the interim evaluation of the EDF confirms that the programme has effectively reduced fragmentation in EU defence research and development (R&D) under a single, coherent framework. Although many projects are still at an early stage and longer-term impacts will only become evident closer to the final evaluation in 2031, the EDF has already demonstrated clear added value by supporting the entire capability development cycle and stimulating cross-border cooperation. This has led to greater efficiency and innovation, particularly among smaller and non-traditional stakeholders. The Commission has continuously refined implementation based on stakeholder feedback, resulting in simplified procedures and improved outreach, though further improvements are still required, especially in co-financing and procurement certainty.

The EDF is on course to meet its medium- and long-term goals, with over 50 next-generation prototypes expected across all military domains. It also contributes to reducing European dependence on third-country technologies, with some products already entering service in Member States and in Ukraine. Stakeholders regard the EDF's priority-setting tools as relevant and well aligned with other EU and national initiatives, with NATO standards reinforcing interoperability. The programme's capacity to fund projects that individual Member States could not pursue alone is widely acknowledged, as is its responsiveness to emerging challenges and policy shifts.

Looking ahead, the evaluation highlights several areas for further improvement. These include better continuity between R&D, industrialisation and procurement, faster and leaner funding cycles, stronger support for innovation and newcomers, and closer integration with ongoing EU policy initiatives. According to the results, efficiency could be further enhanced by addressing challenges in co-financing, simplifying administrative procedures and ensuring secure and streamlined information exchange. Greater coherence could be achieved through deeper cooperation with the EDA and the EEAS, better alignment with PESCO projects, and enhanced civil-defence synergies. In view of heightened geopolitical instability and growing demand from Member States and industry, a future increase in EDF funding is recommended. Additionally, Ukraine's participation in defence R&D should be strengthened. Finally, the report underlines the need to improve monitoring and reporting, ensuring that programme impacts are captured effectively while avoiding excessive administrative burden, aided by smarter use of digital tools and collaboration with the EDA and Eurostat. According to the Commission proposal, the next MFF for 2028-2034 aims to allocate €131 billion to defence, security, and space, a fivefold increase compared to the previous MFF.

Tackling fragmentation and enhancing cooperation

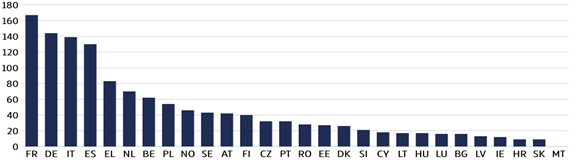

By March 2025, the Commission had adopted five annual EDF work programmes, committing a total of €5.4 billion to collaborative defence research and capability development (around €6 billion including the precursor programmes EDIDP and PADR). According to the Commission, this makes the Fund one of the three largest sources of defence R&D investment within the EU; approximately half of all collaborative defence research at EU level is now financed through the EDF. Despite these efforts, an expert from the Fondation Robert Schuman notes that, with the current budget, the EU 'remains a secondary player'. By supporting collaboration and shared working practices, the EDF helps to reduce fragmentation within the EDTIB. To date, 162 projects have been supported under the EDF, involving 1 366 distinct participants from 26 Member States and Norway.

| Entity | Country | Projects |

|---|---|---|

| Thales | France | 85 |

| Leonardo | Italy | 60 |

| Indra | Spain | 53 |

| Fraunhofer | Germany | 48 |

| Saab | Sweden | 42 |

| TNO | Netherlands | 41 |

| Safran | France | 35 |

| Austrian Institute of Technology | Austria | 34 |

| Rheinmetall | Germany | 34 |

Source: Fiott, 2025.

In the 2021 round, the 61 selected collaborative defence R&D projects were awarded a total of €1.2 billion in funding. The successful proposals involved 18 entities from eight EU Member States and Norway, on average, and half of the selected capability development proposals will be established within the PESCO framework. In the 2022 round, €832 million was invested in 41 defence projects, with an average of 22 entities from nine EU Member States and Norway participating per project, with 11 of the selected proposals linked to PESCO.

Third-country participation in the EDF

The EDF primarily funds entities based in the EU or Norway (as an associated country), but allows subsidiaries of third-country companies to participate if the host Member State guarantees European control over management, intellectual property, sensitive information and export decisions. Recipients of EDF funding must be EU-based (or in an associated country), with their executive management based in the EU; they cannot be controlled by a non-associated third country. However, exceptions are possible through approved guarantees. For instance, Avio Aero (based in Italy but a subsidiary of the US company General Electric's GE Aviation) participates in the EU Next Generation Rotorcraft Technologies Project (ENGRT) and Novel Energy and Propulsion Systems for Air Dominance (NEUMANN). Coordination with a third-country entity is possible if it is not against the Union's security interests, although these are not eligible for EDF funding.

According to an expert, two features of the EDF explain the strict rules: first, its exclusive focus on defence R&D, which generates sensitive intellectual property; second, its long-term strategic orientation, aimed at enhancing EU strategic autonomy rather than addressing immediate operational needs.

The results of the third EDF work programme – for 2023, with another €1 billion in funding – involve an average of 17 entities from eight Member States, with 14 projects linked to PESCO. The results of the fourth (2024) EDF call will lead to the EU investing €910 million in 62 projects with an average of 15 entities from seven different countries participating in each of the projects and 13 projects being linked to PESCO. While the minimum requirement for EDF participation is three legal entities from three different Member States or Norway, the average project now brings together 19 entities from eight countries. To improve these results even further, experts from the Centre for European Policy Studies (CEPS) note: 'the European Commission should raise the bar for EDF eligibility from the current "three entities from three Member States" rule. The involvement of more Member States would lead to the better integration of armaments supply chains ... which would subsequently allow for improvements in interoperability.' This could be further encouraged by providing an EDF bonus for the joint operation of commonly developed equipment. CSIS experts and an Egmont analyst suggest significantly expanding the size of the EDF, given the huge future needs.

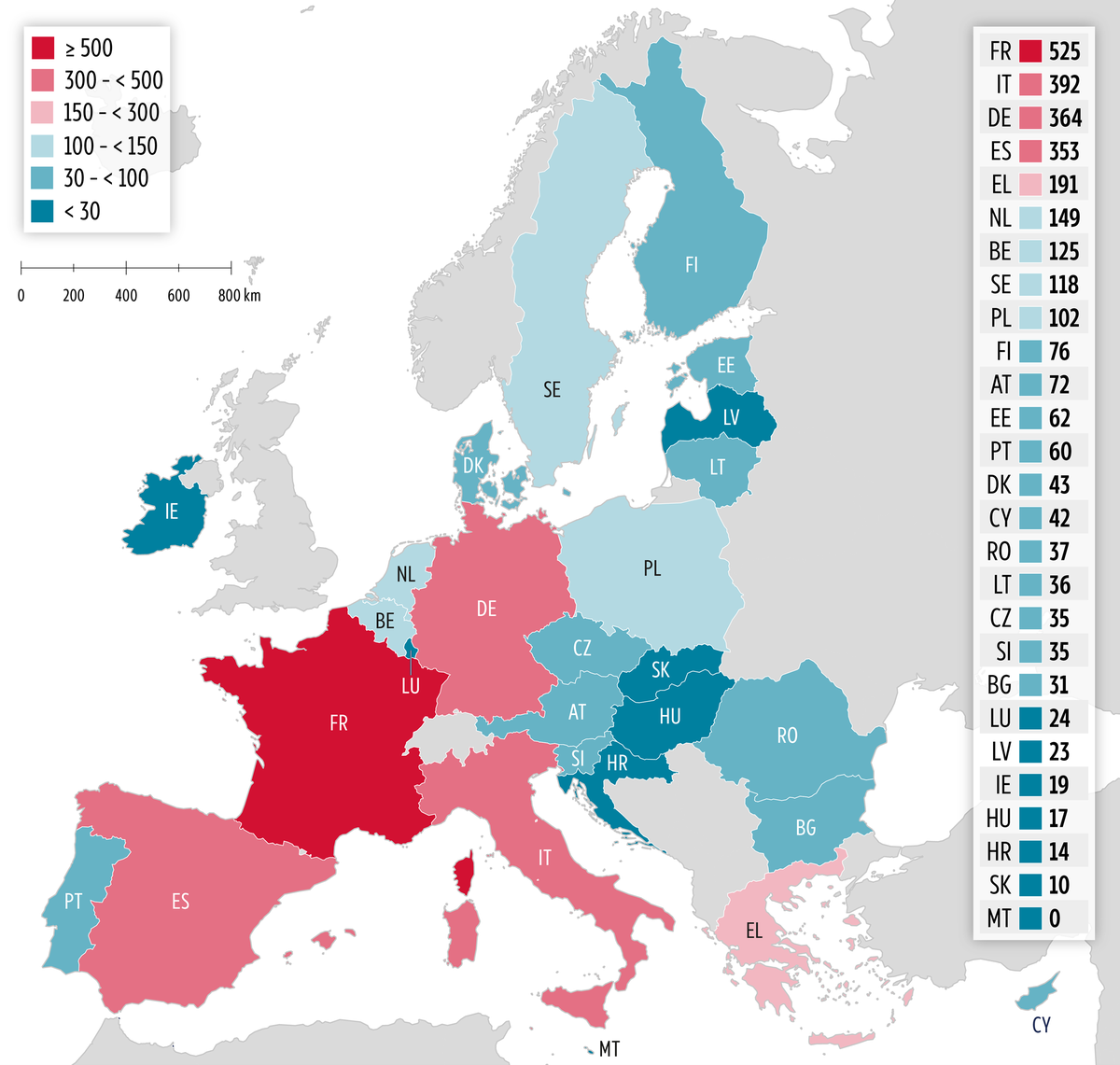

Source: Fiott, 2025; diagram by the author. Graphic by: Lucille Killmayer. Note: Malta does not participate in any EDF projects.

Participants include a broad geographical range of organisations, including those located in areas without a strong tradition of defence industry activity. Legal entities from Member States with long-established defence sectors continue to receive the largest shares of EDF funding, which reflects the scale of their national defence markets (see Figure 1).

French participants are involved in more EDF projects than those of any other Member State, followed by Germany, then Italy and Spain. However, according to the Commission, even medium-sized and smaller Member States with more limited defence industrial capacity have benefited significantly. In the first year of operation alone, EDF support equalled or surpassed total national defence R&D spending in 15 Member States. Indeed, the data also indicate growing involvement of Member States with a smaller defence industrial base in EDF projects. Cyprus, for instance, saw the number of participating entities rise from 15 in 2021 to 24 in 2024.

According to an expert from the Fondation Robert Schuman, countries with established defence industries such as France, Spain, Greece, Italy and Germany have unsurprisingly emerged as the primary beneficiaries of EDF allocations and project coordination. Nonetheless, the Commission has also entrusted coordination roles to states with limited or nascent defence sectors, including Romania, Slovenia, Portugal, Ireland and Cyprus. The expert provides three potential explanations. One possible explanation lies in the Commission's enduring commitment to fostering competition, including efforts to support smaller actors alongside major industrial players. Encouraging new entrants into the defence market aligns with the objective of promoting innovation and avoiding monopolisation by established firms. A second interpretation suggests that the Commission may be using EDF budgetary instruments to help shape a more diversified European defence industrial landscape. The evolution of contemporary warfare, marked by the convergence of advanced technology and cost-effectiveness, arguably creates space for new industrial players. Rather than merely allocating contracts, the EDF could thus be seen as a tool to cultivate defence capacities wherever they can viably emerge. A third hypothesis highlights the political logic underpinning project selection. Ensuring broad participation among Member States reflects the EU's longstanding tendency to balance effectiveness with inclusivity. This rationale echoes earlier compromises seen in initiatives such as PESCO, where debates over exclusivity versus inclusiveness similarly shaped the outcome. The role of the EDF's selection committee in reinforcing this balance-oriented logic is likely to be significant.

Source: European Commission, 2025; Graphic by Lucille Killmayer, EPRS.

The EDF has also proven attractive to a wide range of non-traditional defence actors, with SMEs, mid-caps and research institutions increasingly integrated into the programme. SMEs in particular are gaining prominence as flexible contributors of innovative and potentially disruptive technologies in the defence sector. Due to specific efforts to support their participation and strengthen the commercial and technological maturity of their innovations, SMEs are now heavily involved across the EDF. They account for 43 % of all unique participants and receive approximately 20 % of total funding. In six Member States, SMEs represent over half of all project participants. Mid-caps currently make up 4 % of participants and receive around 6 % of EDF funding.

According to Daniel Fiott, the notion that EU-level institutions such as the European Commission are incapable of overseeing defence-related initiatives in cooperation with Member States is no longer tenable. While the governance of joint defence procurement remains more complex than the management of innovation projects, publicly available data published by the Commission since 2021 suggests that the EU has established a distinct model for supporting defence research and development. This model brings together the Commission, Member States, defence industries and research organisations in new and cooperative ways. The Fund has clearly fostered a deeper level of pan-European collaboration in defence R&D, enabling prime contractors, SMEs, technical bodies and research institutions across the Union and its partners to work together in an integrated manner. These developments strengthen the case for an increased financial allocation to the Fund after 2027.

Advancing next-generation capabilities

European Defence Fund priorities

The EDF is managed directly by the Commission through annual work programmes organised into 34 thematic and horizontal categories, aligned with the 2021-2027 MFF. Priorities reflect EU security and defence interests, based on capability needs identified by Member States through the Capability Development Plan and, where relevant, by NATO or regional partners. The programmes cover all military domains and key technologies, aiming to support critical capabilities. They are developed in close cooperation with Member States within the EDF Programme Committee, the EDA and the EEAS.

Expert analysis shows that, since 2021, the Commission has directed EU investment under the EDF towards a broad spectrum of capability areas. These include air combat (2.2 % of projects), air and missile defence (1.7 %), cyber (3.1 %), digital transformation (8 %), disruptive technologies (9.3 %), energy resilience and environmental projects (2.6 %), force protection and mobility (2.6 %), ground combat (5.3 %), information superiority (5.3 %), materials and components (3.5 %), medical and CBRN response (4 %), naval combat (3.1 %), innovation and SMEs (30.2 %), sensors (2.2 %), simulation and training (1.3 %), space (2.6 %), quantum technologies (1.3 %) and underwater warfare (2.2 %). While the largest share of projects by number has fallen under the 'Innovation and SMEs' category, funding distribution tells a different story. The highest financial contributions have been allocated to naval combat (€432.9 million), air combat (€402 million), ground combat (€398.4 million), space (€329.4 million) and information superiority (€328.1 million), reflecting a strategic emphasis on reinforcing core military capabilities.

The EDF, though still in its early implementation phase with no completed projects to date, is addressing critical capability gaps across all operational domains of the EU's armed forces. Drawing on lessons from its precursor programmes and the uptake of early results by Member States' armed forces, the EDF is geared towards fostering collaborative development of next-generation defence technologies. Its design follows a user-centric approach, aligned closely with priorities established through the Capability Development Plan (CDP), the Coordinated Annual Review on Defence (CARD), PESCO, and EDA initiatives, as well as relevant NATO frameworks.

The EDF enables cooperation that would be financially or technically unfeasible for individual Member States, especially in areas such as hypersonic missile defence and major defence platforms. Its financial scale often exceeds national defence R&D budgets, making it a vital enabler of projects like the European Patrol Corvette, Eurodrone, and the EU HYDEF and HYDIS2 interceptors.

Smaller Member States and those with less-developed defence industries also benefit from access to large collaborative projects. In total, EDF-supported initiatives are expected to deliver over 50 prototypes across the air, ground, naval, space and cyber domains, providing critical technology building blocks for the next generation of European defence capabilities.

Recent conflicts have accelerated existing trends in warfare, such as the use of unmanned systems and the growing relevance of air and missile defence, cyber, and space-based capabilities. EDF work programmes have evolved accordingly. For instance, the expansion of funding for air and missile defence and force mobility reflects urgent operational needs. EDF actions are also beginning to support the integration of the Ukrainian defence industry into the EDTIB, albeit with limitations under the current regulation.

Socio-economic returns of the EDF

The EDF is expected to deliver strong economic and societal value, as highlighted by a Joint Research Centre macroeconomic study. Although limited by the early stage of implementation, the study estimates that the EDF could boost EU GDP by up to 0.025 % in 2030, equivalent to €2.95 billion and 32 413 additional jobs. Given that the European defence industry employs around 500 000 people, this suggests a meaningful economic impact. Beyond direct growth effects, the EDF is seen as enhancing innovation, industrial competitiveness and market opportunities, including in dual-use sectors. It also improves the efficiency of R&D by promoting scale, interoperability and reduced duplication across Member States.

Stakeholders involved in the interim evaluation of the EDF noted that EDF projects encourage more ambitious cooperation than would be feasible at national level, enabling the development of complex capabilities and expanding recruitment opportunities for skilled professionals.

A key element of the EDF's added value lies in ensuring continuity across the R&D cycle, bridging the so-called 'valley of death' between research and market uptake. More than half of the earlier EDIDP projects have continued under the EDF, and many current projects now include provisions for next-stage funding. However, the availability of sufficient co-financing remains a challenge. Development projects depend on national co-financing commitments, which are increasingly difficult to secure, often delayed by complex negotiations over memoranda of understanding and user rights.

For instance, according to one expert, in Italy's case, even where industrial potential is strong, delays in securing national commitments limit the capacity to sustain momentum. This reinforces the point that national engagement is essential not only for initial participation but for maintaining project continuity within the EDF framework. Thus the expert recommends that, to improve Italy's performance in EDF calls, the Italian Ministry of Defence must play a more active coordinating role – both by supporting SMEs, which make up a high share of Italian participation, and by encouraging national industry to lead consortia. He argues that, despite the EDF's supranational design, national authorities still exert significant influence and must ensure strategic alignment, enable follow-up funding, and reduce procedural barriers to maximise Italy's industrial potential.

The EDF's success depends on the procurement of developed capabilities by Member States. Initial results show that EDF-backed systems are already being adopted by EU armed forces and deployed in operational settings, including in Ukraine. For instance, the iMUGS project, funded under the EDIDP, enhances the autonomous functions of existing platforms to support a wide range of operational tasks. These upgraded platforms are actively used in Ukraine for clearing minefields, evacuating casualties and transporting supplies. In parallel, the AI4DEF project has delivered autonomous surveillance and threat detection solutions that are currently employed by the Ukrainian armed forces. The European Patrol Corvette project is developing a versatile corvette-class vessel for future maritime operations. Four Member States (France, Italy, Spain and Greece) have confirmed procurement interest, with some already allocating national funding.

Defence innovation

The EDF has made innovation a strategic priority, particularly in disruptive technologies. The EDF regulation specifically allocates 4 % to 8 % of the EDF annual budget to emerging disruptive technologies. For instance, a next-generation electro-optical sensing device is being developed with EDF funding.

The EU defence innovation scheme (EUDIS) is a dedicated initiative under the EDF aimed at supporting innovative defence solutions, particularly from start-ups and SMEs. It combines EDF grants with public and private investment to mobilise around €2 billion by 2027. In 2024, €225 million was allocated to EUDIS actions, including innovation challenges, civil-to-defence technology transfer, and coaching services. EUDIS combines conventional R&D support with new instruments aimed at boosting innovation, and aims to strengthen the defence innovation ecosystem by lowering entry barriers and accelerating the market uptake of disruptive technologies. Additional EUDIS support is geared towards start-ups and SMEs through hackathons, coaching, matchmaking and the Defence Equity Facility, administered via the European Investment Fund (EIF). In 2024, the EDF is allocating over €224 million to support defence innovation and SMEs through EUDIS, including €52 million dedicated to two specific technological challenges.

Launched in January 2024, the €175 million Defence Equity Facility (DEF) is managed by the EIF on behalf of the European Commission's Directorate-General for Defence Industry and Space (DG DEFIS). Its purpose is to back venture capital and private equity funds investing in European firms developing innovative defence technologies with dual-use potential, in line with the EIF's exclusion policy. The facility is funded through €100 million from the EDF and €75 million from the EIF, with a four-year investment window running until 2027. It aims to mobilise up to €500 million in total investment, including private capital, and is part of the European Investment Bank Group's broader effort to advance EU security and defence goals, alongside initiatives like the Strategic European Security Initiative.

The experience of Ukraine has underscored the importance of agile innovation, battlefield-tested feedback loops and rapid delivery. Ukraine's war effort has emerged as a striking example of how urgency drives technological innovation. Confronted with a more powerful and better-equipped opponent, the country has developed a defence-tech ecosystem that is redefining contemporary warfare. The EDF is now under pressure to adapt its processes to support more flexible, fast-track innovation while maintaining its long-term focus on capability development.

An EU Defence Innovation Office was launched in Kyiv in September 2024. It aims to strengthen cooperation between the EU and Ukraine by promoting joint defence innovation initiatives, facilitating access to EU programmes, and supporting Ukraine's integration into the European defence industrial framework. Furthermore, BraveTech EU, a joint initiative of the European Commission and Ukraine announced at the Ukraine Recovery Conference 2025, aims to deepen defence industrial cooperation by linking Ukraine's battlefield-tested innovation with EU programmes such as the EDF and EUDIS, fostering joint technology development, rapid testing and integration of start-ups and SMEs in support of European security and the Readiness 2030 agenda. BraveTech EU will launch with support from the EDF and EUDIS, aiming to mobilise up to €50 million in EU funding to match Ukraine's €50 million contribution, thereby reinforcing joint defence innovation efforts.

The EDF operates within a broader EU effort to strengthen technological sovereignty and address critical dependencies through coordinated innovation and targeted investment. Back in February 2021, the Commission put forward an action plan on synergies between defence, space and security, which seeks to increase complementarity between relevant EU programmes such as Horizon Europe and the EDF, to profit from the disruptive potential of technologies at the intersection between space, defence and civil uses.

On 15 February 2022, the Commission adopted a roadmap on critical technologies for security and defence outlining how the EU can enhance research, technology development and innovation in critical technologies and how to reduce strategic dependencies. In May 2022, the EDA launched the Hub for EU Defence Innovation (HEDI) within the EDA to foster innovation and collaboration with Member States.

The Observatory on Critical Technologies identified key risks in autonomous systems and electronic components, prompting the development of targeted technology roadmaps in 2023. A first classified report with detailed findings on electronic components has been published, with a second forthcoming. These analyses inform mitigation strategies aimed at safeguarding EU defence, space and civil value chains from technological dependencies and supply chain vulnerabilities.

In February 2024, the EU agreed to establish the Strategic Technologies for Europe Platform, including €1.5 billion under the EDF – earmarked for the forthcoming EDIP – to reinforce technological sovereignty and bolster firms developing critical capabilities. In the White Paper on European Defence/Readiness 2030, the Commission announced that it will present a European armament technological roadmap on investment into dual-use advanced technological capabilities in 2025.

European Parliament position

The European Parliament, as co-legislator, adopted the Regulation on establishing the EDF. Parliament regards the EDF as a key instrument for strengthening EU defence capabilities and industrial cooperation, consistently calling for its full use, increased funding, and better integration with other initiatives such as PESCO, CARD and EDIRPA.

Parliament has expressed regret over past budget reductions to the EDF and has stressed its added value despite being underfunded. It has highlighted the EDF's role in remedying capability gaps, fostering innovation and supporting technological autonomy, while emphasising the need for coordinated investment to avoid duplication and ensure strategic impact.

MEPs stress the need for full parliamentary oversight to ensure that increased defence spending aligns with EU strategic goals and security interests, and have reiterated calls for delegated acts for the work programmes of EU-funded defence industrial programmes.

Parliament stresses that the EDF must be utilised fully and coherently with other EU instruments to enhance EU defence capabilities, and highlights that effective capability development depends on aligning EDF-supported projects with jointly defined military requirements. Parliament also calls for greater flexibility and speed in EDF funding cycles, especially in support of disruptive technologies.

Main references

- European Commission, Interim evaluation of the European Defence Fund, June 2025.

- Fiott, D., Defence Innovation Trends: A Data Snapshot of the European Defence Fund, May 2025.

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.