Article page checkbox is not checked in page info.

Taxation omnibus

Omnibus on Taxation Revising EU rules on direct taxation: implementation takeaways

Mafalda Monda and Hannah Ahamad Madatali, Ex-Post Evaluation Unit

Key findings

As part of ongoing European Union (EU) efforts to create a more business-friendly and competitive environment, on 24 June 2026 the European Commission presented a proposal for a tax simplification package, including an omnibus simplifying EU rules on direct taxation. The proposed omnibus comprises a set of measures designed to streamline EU direct taxation rules and reduce administrative burdens, by revising key corporate tax directives. The legislative acts proposed for revision are the Interest and Royalties Directive, the Tax Merger Directive, Parent-Subsidiary Directive, the Anti-Tax-Avoidance Directive, the Tax Dispute Resolution Mechanisms Directive, and the Faster and Safer Relief of Excess Withholding Taxes Directive. The implementation of this legislation has led to a fragmented landscape across EU Member States, characterised by different rules and interpretations. Evidence indicates that these directives have created significant challenges for taxpayers and businesses, leading to legal uncertainty and inefficiencies, particularly for cross-border activities, which can undermine the proper functioning of the EU single market and business competitiveness. Additionally, the tax landscape has evolved significantly, both within the EU and globally, since the adoption of the directives the omnibus addresses. This evolution is particularly evident with the introduction of new regulations such as the EU's Global Minimum Tax Directive, which has created additional complexities in the existing tax framework. This implementation appraisal focuses primarily on the revision of the directives under the omnibus. It also examines implementation reports, evaluations, and other evidence assessing the application of the directives under revision. It summarises the main features of the omnibus proposal and considers the European Parliament's perspective, written questions from its Members, and the views of stakeholders, including EU institutions and advisory bodies.

Purpose statement

This briefing is one in a series of implementation appraisals produced by the European Parliamentary Research Service (EPRS) on the operation of existing EU legislation in practice. Each briefing focuses on a specific EU law that is announced to be amended or reviewed in the European Commission's annual work programme. Implementation appraisals aim at providing a succinct overview of publicly available material on the implementation, application and effectiveness to date of that specific EU law, drawing on input from EU institutions and bodies, as well as external organisations.

Background and existing EU policy framework

According to the European Central Bank (ECB), taxation policies and particularly inefficient withholding tax procedures1 and double taxation, create significant barriers for cross-border investment and hinder the integration of capital markets across the European Union (EU). The EU has legislation in place to ensure fair taxation, prevent tax avoidance and facilitate cross-border activities in its internal market. The EU's legislative framework includes measures to prevent double taxation on cross-border payments such as dividends, interest and royalties. It is complemented by other measures aiming to prevent aggressive tax planning2 and resolving cross-border disputes.

However, the implementation of this legislation has led to a fragmented landscape characterised by different rules and interpretations across EU Member States. This resulted in challenges for taxpayers and businesses, who consistently emphasise the need for greater simplification of the EU corporate tax rules to support competitiveness and the functioning of the EU single market. Additionally, the introduction of the global minimum tax regime under Council Directive (EU) 2022/2523 (Pillar 2 Directive)3 has significantly modified the context in which various EU anti-abuse provisions function.

The European Commission's 2024-2029 Political Guidelines set the objective to create a more business-friendly environment in the EU by reducing administrative burdens and simplifying the implementation of regulations, making it easier for businesses to operate within the EU. Specifically, the Commission has committed to reduce administrative burdens by the end of its mandate by a minimum of 25 % for all businesses, and by at least 35 % for small and medium-sized enterprises (SMEs). In October 2025, the Commission presented its 2026 work programme, mentioning a new 'omnibus'4 initiative to simplify and streamline the EU taxation rules.

The proposed omnibus was presented on 24 June 2026, as part of a 'tax simplification package' that includes the revision of the Directive on Administrative Cooperation (DAC) (2011/16/EU).5 Of the two initiatives included in the package, only the omnibus was included in one of the Commission's work programmes. The omnibus states it aims to ensure that the EU's direct tax framework 'remains coherent, proportionate and effective'. In its proposal, the Commission proposes to revise the following corporate tax directives:

-

the Interest and Royalties Directive (IRD) (2003/49/EU);

-

the Tax Merger Directive (TMD) (2009/133/EU);

-

the Parent-Subsidiary Directive (PSD) (2011/96/EU);

-

the Anti-Tax-Avoidance Directive (ATAD) (2016/1164/EU as amended by 2017/952/EU);

-

the Tax Dispute Resolution Mechanisms Directive (DRM) (2017/1852/EU);

-

and the Directive on Faster and Safer Relief of Excess Withholding Taxes (FASTER) (2025/50/EU).

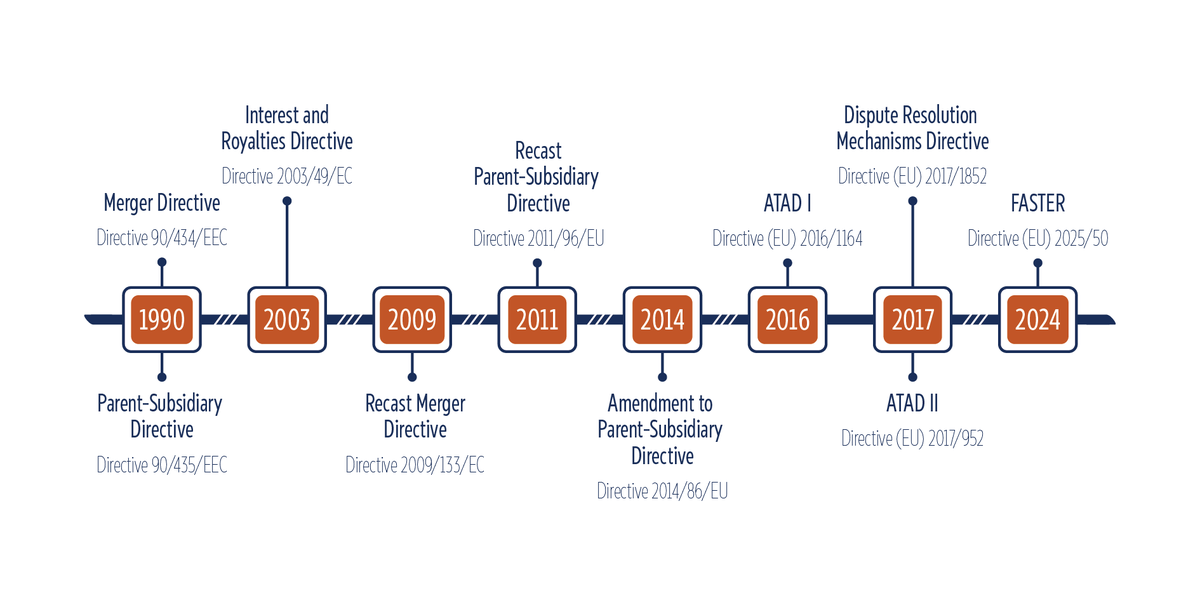

The timeline for the EU's adoption of the above-mentioned directives is provided in Figure 1.6

EU corporate tax directives

Source: Authors' elaboration; graphic by Nadejda Kresnichka-Nikolchova, EPRS.

Interest and Royalties Directive (IRD)

The IRD was adopted in June 2003, and Member States were required to transpose it by January 2004. Its objective is to eliminate double taxation and reduce compliance costs by exempting qualifying cross-border intra-group interest and royalty payments from withholding tax in the Member State of source (Article 1(1)). The exemption applies only where the recipient is the beneficial owner of the payment and is either a company in another Member State that is associated7 with the payer or a permanent establishment of such a company situated in another Member State (Articles 1(1), 1(4), 1(5), 1(7) and 3(a)–(c)).

Tax Merger Directive (TMD)

The TMD entered into force in December 2009 and aims to remove tax obstacles to cross-border companies' reorganisation involving companies from two or more EU Member States. It establishes a common system of taxation for mergers, divisions, partial divisions, asset transfers and exchanges of shares to ensure that they are tax neutral,8 and do not lead to double taxation. The directive also applies to the transfer of registered offices of European companies (SEs) and European cooperative societies (SCEs) (Articles 1(b) and 12‑14). Its main provisions include the deferral of taxation on capital gains until realisation (Article 4), and the transfer to the receiving company's permanent establishment of provisions or reserves that are wholly or partly exempt from tax under the same conditions as would have applied to the transferring company (Article 5). The directive was amended in 2013 following Croatia's accession to the EU, to add Croatian company forms and the corresponding tax to the Annex I list of qualifying companies and taxes.

Parent-Subsidiary Directive (PSD)

The PSD was adopted in November 2011 and entered into force in January 2012. It aims to simplify taxation of groups of companies operating within the EU. The PSD prevents the double taxation of profits distributed by subsidiaries to their parent companies by requiring Member States either to exempt such profits from taxation or to grant relief for the underlying corporate tax paid by the subsidiary (Article 4(1)). In addition, the directive exempts qualifying profit distributions made by subsidiaries from withholding tax in the Member State of source (Article 5). However, to qualify for these benefits, the parent company must be resident in an EU Member State and hold at least 10 % of the capital of a subsidiary established in another Member State (Article 3(1)(a)).

The directive was amended in 2014 to prevent double non-taxation arising from hybrid loan arrangements (Article 4(1)(a). Other measures include provisions relating to the treatment of management costs and other expenses related to holding (Article 4(3)) and exemption from withholding tax on profits distributed by subsidiaries (Article 5(1)). In 2015, a general anti-abuse rule was introduced to combat tax avoidance and ensure fair taxation by preventing the directive's benefits from being granted to non-genuine arrangements (Article 1(2)‑(4)).

Anti-Tax-Avoidance Directive (ATAD)

The ATAD was adopted in July 2016 and introduces legally binding anti-abuse measures that all Member States must implement to counter common forms of aggressive tax planning. The ATAD sets out five key provisions to close loopholes frequently exploited for tax avoidance with the purpose to establish a minimum level of protection against corporate tax avoidance within the EU. These measures9 include the interest limitation rules (Article 4), which discourage debt arrangements designed to minimise taxation, and the exit taxation rules (Article 5), which prevent companies from avoiding taxes when relocating assets.

Furthermore, controlled foreign company rules (CFC, Articles 7-8) aim to prevent profit-shifting to controlled entities located in low-tax jurisdictions by allowing certain undistributed income of those entities to be taxed at the level of the parent company. The general anti-abuse rule (GAAR) aims to enable Member States to disregard non-genuine arrangements put in place primarily to obtain a tax advantage where more specific anti-abuse rules do not apply (Article 6). The hybrid mismatch rules (Article 9) aim to prevent companies exploiting national mismatches to avoid taxation.

Tax Dispute Resolution Mechanisms Directive (DRM)

Multilateral Convention on the International Tax Dispute Resolution Commission (ITDRC)

In May 2026, 10 EU Member States (Austria, Bulgaria, Denmark, France, Germany, Ireland, the Netherlands, Poland, Spain, and Sweden) finalised technical negotiations. The resulting Convention is intended to provide permanently available panels to conduct the arbitration phase of mutual agreement procedures more swiftly and efficiently. The Convention will be open for other States to join. This new convention and coalition of the willing builds on earlier work by a FISCALIS working group exploring options to establish a Standing Committee on Alternative Dispute Resolution under Article 10(1).

The DRM entered into force in November 2017 and applies to any complaint submitted from 1 July 2019 onwards relating to disputes concerning income or capital earned in a tax year commencing on or after 1 January 2018. The DRM aims to streamline the resolution of tax disputes concerning the interpretation and application of agreements and conventions providing for the elimination of double taxation of income and, where applicable, capital (Article 1). Specifically, the directive addresses double taxation issues arising from conflicting national rules or differing interpretations of tax treaties. The directive establishes clear deadlines for resolving tax disputes through the Mutual Agreement Procedure (MAP), including rules on the submission and admissibility of complaints and the time limits for reaching an agreement (Articles 3‑6). It also grants taxpayers access to national courts will competent authorities fail to take decisions on admissibility of a complaint and allows them to request a dispute resolution body is established (Articles 5(3), 6(1) and 7(1)).

Faster and Safer Relief of Excess Withholding Taxes Directive (FASTER)

FASTER, which was adopted in December 2024 and entered into force in January 2025, will apply in Member States from 1 January 2030. The directive aims to make withholding tax relief procedures faster, safer and more efficient for cross-border investors within the EU. FASTER introduces a common EU digital tax residence certificate (eTRC), enabling taxpayers to prove their tax residence electronically (Article 4). The directive also establishes national registers of certified financial intermediaries (Article 5) and lays down the rules governing their certification and registration (Articles 6‑9). It also introduces two accelerated procedures for obtaining relief from excess withholding tax: a relief-at-source system and a quick refund system (Articles 11‑14). To reduce fraud and abuse, FASTER introduces standardised reporting obligations for certified financial intermediaries (Article 10). In addition, registration requests and Member State decisions concerning the registration, rejection or removal of certified financial intermediaries are transmitted or recorded electronically through the European Certified Financial Intermediary Portal10 (Article 6).

European Commission reports, studies and consultations in preparation of the revisions

The Anti-Tax-Avoidance Directive (ATAD) is the only directive among those to be revised under the omnibus package that has been subject to a comprehensive evaluation, in accordance with the Commission's Better Regulation framework. The Commission also published an implementation report in August 2020, as required by Article 10 of the directive. This report assesses implementation of the ATAD, with particular emphasis on the operation of the interest limitation rule under Article 4. As several ATAD provisions had only recently become applicable, the report was based on limited implementation experience. The Interest and Royalties Directive (IRD) was the subject of an implementation report in 2009, as required by Article 8 of the Directive. No comparable Commission implementation reports or evaluations were carried out on the Tax Merger (TMD) and Parent-Subsidiary (PSD) directives. The Tax Dispute Resolution Mechanisms Directive (DRM) contains an explicit evaluation obligation (Article 21), requiring the Commission to evaluate its implementation by 30 June 2024 and present a report to the Council, accompanied by a legislative proposal where appropriate. To date, however, the Commission has only published an implementation report on the review of the directive (October 2024), while no comprehensive Better Regulation evaluation has been carried out. The FASTER directive establishes reporting and evaluation obligations, but these will only become applicable after its transposition deadline, and the first evaluations are not due until 2032 and 2034.

European Commission evaluation of the Anti-Tax-Avoidance Directive

In July 2024, the Commission launched a call for evidence for its evaluation of the ATAD, which was open for feedback from stakeholders between July and September 2024. The consultation received 49 responses, predominantly from business stakeholders. Business associations accounted for approximately 39 % of all respondents, followed by individual companies and businesses (approximately 22 %), and EU citizens (14 %). The remaining responses were submitted by a range of other stakeholders including public authorities, research institutions, non-EU citizens, non-governmental organisations (NGOs) and academia. Responses were submitted by stakeholders from 12 Member States, two non-EU countries (the United Kingdom and the United States) and one overseas country and territory (Bonaire, Sint Eustatius and Saba). Stakeholders supported the ATAD objectives but highlighted the need to simplify and harmonise its provisions, particularly considering Pillar 2, pointing to divergent national implementation, excessive compliance costs and the impact of certain rules, notably the interest limitation rule, on investment and competitiveness.

Additionally, the evaluation drew on evidence collected through targeted consultation activities carried out in the context of a supporting study commissioned by the Commission. First, all 27 Member State tax authorities were consulted through a combination of in-depth interviews and an email survey to gather evidence on ATAD implementation and application and its performance against the evaluation criteria. Second, private stakeholders – including tax advisers, multinational enterprises, business federations, academics and NGOs – were consulted through interviews and a web-based survey to capture practical experience with the directive's application, its impact on taxpayer behaviour and compliance costs, and implementation challenges. Finally, the preliminary findings of the supporting study were presented and discussed at meetings of the Platform for Tax Good Governance and the Working Party IV.

The evaluation was published in June 2026, alongside the omnibus, and draws on the findings of the external study. The evaluation assessed the ATAD against the five Better Regulation criteria (effectiveness, efficiency, relevance, coherence and EU added value). It examined the ATAD's implementation across the Member States, including the policy choices made where the directive allows for flexibility. It also assessed the directive's effectiveness in addressing aggressive tax planning, whether its implementation has delivered added value compared with what could have been achieved by Member States acting individually, and its continued relevance, particularly considering the adoption of the Pillar 2 Directive.

Key findings of the evaluation highlight that, while ATAD successfully reduced fragmentation in anti-tax-avoidance rules in Member States, the flexibility provided to Member States on implementation options led to divergent national approaches, creating complexity and legal uncertainty for businesses. The ATAD interest limitation rule (Article 4) is identified as the most impactful, though stakeholders note it is insufficiently targeted and has become outdated. The evaluation found no significant impact of the exit taxation rule (Article 5) had minimal effect on tax-base protection, while though necessary, the GAAR (Article 6) introduces legal uncertainty due to vague scope and interpretation challenges. Additionally, the deterrent effect of the CFC rule (Articles 7‑8) is acknowledged, but its administrative burden is significant, particularly with the introduction of Pillar 2. Though effective when applied, the hybrid mismatch rule (Article 9) is complex, especially regarding imported mismatches.11

However, while the ATAD has strengthened the protection of tax bases, its efficiency is constrained by significant compliance costs, limited evidence on benefits, and data gaps that prevent a robust cost-benefit assessment. The evaluation also finds that the ATAD remains highly relevant, as cross-border tax avoidance continues to pose significant challenges. In terms of EU added value, the directive has established legally binding minimum anti-avoidance standards across all Member States, reducing regulatory fragmentation and creating a more level playing field than could have been achieved through voluntary international standards alone. The ATAD is generally coherent with the broader EU and international tax framework. Nevertheless, differences in national implementation and emerging interactions with the Pillar 2 rules have increased legal complexity, pointing to a need for further harmonisation and simplification.

The evaluation concludes that legislative amendments and administrative guidance are needed to address the fragmentation witnessed following the ATAD's implementation, and to better balance costs and benefits. This could also support broader EU policy priorities, such as enhancing competitiveness by removing tax barriers to cross-border business activities.

Stakeholder consultation

In February 2026, the Commission launched a call for evidence for an impact assessment12 of the omnibus proposal, which ran from February to March 2026 and received 117 replies from stakeholders from 18 Member States and 5 contributions from stakeholders in Albania, India, Kenya, the United Kingdom and the United States. Respondents included business associations (46 %), private businesses (23 %), EU citizens (9 %), and NGOs (5 %). The remaining responses were submitted by other entities, including public authorities, research institutions, and non-EU citizens. Stakeholder replies showed a broad consensus that the omnibus should not only focus on removing isolated reporting obligations, but also improve the coherence, proportionality and practical usability of the EU's direct taxation acquis. Approximately 77 % of stakeholders who replied called for enhanced harmonisation and reduced national discretion in the directives' implementation. Around 50 % suggested standardising procedures, including the use of digital tools, and 60 % emphasised the importance of simplifying rules for SMEs.

Across respondents, there were consistent calls for fewer overlaps, greater alignment between directives, less flexibility for Member States to apply provisions offering exemptions or relief, more predictable procedures and better coordination with the EU's Pillar 2 framework. Specifically, concerning the IRD and PSD, 67 % of stakeholders highlighted the need to simplify the withholding tax framework, to address complexity, strict eligibility requirements, and inconsistent application. Additionally, stakeholders noted the ATAD's complexity and suggested addressing its parallel application with Pillar 2. Regarding the TMD, 38 % of stakeholders called to extend and update its scope, and to align the directive with EU company law and modern business practices. Finally, 38 % of stakeholders found dispute resolution under the DRM slow and complex, suggesting enhancements such as stricter timelines, a permanent arbitration body, and extending the scope to Pillar 2 disputes.

The Commission did not organise an open public consultation as part of the impact assessment. It relied on targeted stakeholder consultations involving Member States through the Council Working Party on Tax Questions, tax administrations, business organisations, professional associations, tax practitioners and academic experts, complemented by an in-depth study on ATAD. These consultations focused on identifying practical implementation issues, sources of administrative burden and opportunities to simplify existing EU corporate tax directives. The Commission also drew extensively on evidence from previous consultations, evaluations and implementation experience relating to the existing directives, particularly the ATAD, the DRM and the recently adopted FASTER Directive. Additional evidence was drawn from economic analysis and statistical data.

Proposal on 'simplifying EU rules on direct taxation – omnibus'

On 24 June 2026, the Commission published its taxation omnibus. The proposal aims to modernise and streamline the EU's direct tax framework to reduce compliance burdens, enhance legal certainty, and support cross-border investment. This would be achieved by amending the IRD, TMD, PSD, ATAD, DRM and FASTER tax directives. The proposed changes are summarised in Figure 2.

European Parliament position and oversight activities

Parliamentary resolutions

During the previous (9th) legislative term, the European Parliament adopted several resolutions that highlight the importance of a fair and efficient tax system, alongside coordinated and simplified corporate taxation rules to ensure a level playing field for businesses across the EU.

In December 2023, the Parliament adopted a resolution on 'Further reform of corporate taxation rules' which emphasises the need for a common approach to tax policies to address harmful tax competition and tax avoidance. It also stresses the importance of reducing the administrative burden on businesses, particularly SMEs, and promoting a fair and efficient tax system. In this context, it refers to the main elements of the existing EU corporate tax acquis, including the ATAD, the PSD, the DRM and the IRD, and calls for the continued review and coherent implementation of existing corporate tax framework to identify opportunities for simplification, reduce administrative burdens, and improve the functioning of the Single Market.

In March 2022, the Parliament adopted a resolution on 'Fair and simple taxation supporting the recovery strategy', emphasising the need for a fair, efficient, and simple tax system to support the EU's economic recovery following COVID‑19. The resolution stresses the importance of a coordinated approach to taxation at EU level, where Member States work together to address tax challenges. The resolution recognises the significance of the ATAD as a key tool in the fight against tax avoidance and aggressive tax planning and calls the Commission to report on its implementation and to relaunch the revision of the IRD. Furthermore, the resolution welcomes the DRM as a tool for resolving tax disputes between EU Member States, calling on the Commission to report on its implementation and effectiveness.

In October 2021, the European Parliament adopted a resolution entitled 'Reforming the EU policy on harmful tax practices (including the reform of the Code of Conduct Group)', calling for a reform of Code of Conduct on business taxation (CoC). The CoC is currently a soft-law instrument aimed at preventing harmful tax competition, but the Parliament believes it needs to be strengthened. In its resolution, the Parliament references several key EU directives, including ATAD, IRD, and PSD. The Parliament welcomes the OECD/G20 agreement on a global minimum tax rate of at least 15 % and calls for the EU to implement the OECD's Pillar 2 proposal on minimum effective taxation. The Parliament also recommends revising the CoC to include a minimum effective tax rate criterion.

The European Parliament's Subcommittee on Tax Matters (FISC) has been entrusted with preparing Parliament's opinion on the proposed taxation omnibus. The opinion will serve as the basis for the Parliament's position to be adopted by the Committee on Economic and Monetary Affairs (ECON). The omnibus proposal is based on Article 115 TFEU, which allows harmonisation of national tax laws that create barriers to the free movement of goods, services, capital, or persons within the internal market. According to this article, the proposal should be adopted under the special legislative procedure, requiring unanimous vote in Council and consultation of the European Parliament and Economic and Social Committee.

Selection of parliamentary questions

A non-exhaustive selection of parliamentary questions from the 7th (2009-2014), 8th (2014-2019) and 9th (2019-2024) terms touch upon the ATAD, the PSD, and the TMD. No parliamentary questions related to the IRD, and the DRM have been identified during this period. The questions selected provide valuable insight into the priorities of Members of the European Parliament regarding these tax directives, highlighting the issues and challenges they raise and the responses the European Commission provided.

Adam Szejnfeld (EPP, Poland) asked whether the Commission would review the ATAD, arguing that some Member States had transposed it more broadly than necessary by extending its application to SMEs and, in some cases, natural persons, whereas he considered it primarily intended to address aggressive tax planning by multinational groups. He also asked how the Commission would address what he considers to be incorrect or excessive national implementation, particularly where it may restrict single market freedoms and create liquidity problems through taxation of unrealised gains (E-005468-18). In its written answer, the Commission replied that the ATAD applies only to corporate taxpayers and sets minimum anti-tax-avoidance standards, while allowing Member States to adopt stricter rules as long as they comply with EU law. It added it would evaluate the directive's implementation, maintained that the exit tax rules are consistent with the freedom of establishment and Court of Justice of the European Union case law, and noted that taxpayers can defer payment of exit taxes over five years when moving within the EU.

Ernest Urtasun (Greens/EFA, Spain) asked the Commission to investigate the CumEx tax fraud scandal, which involved financial institutions claiming tax refunds on dividend returns despite no tax being paid, and to review European rules on parent companies and subsidiaries to prevent such fraud (E-005350-18). In its written answer, the Commission noted it lacks the competence to investigate cross-border tax fraud, which is the responsibility of Member States. The Commission also stated that it does not consider a review of the directive as necessary but noted that it promotes cooperation between tax administrations and supports efforts to combat tax crimes.

A group of European People's Party Members questioned the Commission regarding alleged incompatibility between Article 177 (2) of the Italian Consolidated Tax Act and the TMD (E‑002041‑14), which aims to ensure tax neutrality for corporate reorganisations within the EU. In its written answer, the Commission responded that it lacks competence to assess the compatibility of direct tax provisions only applicable to domestic transactions with EU rules, and it did not see how the different regimes for domestic operations could restrict freedom of establishment or introduce discrimination against foreign companies established in Italy. The Commission concluded there was no violation of the principles laid down in the directive and therefore has no plans to address the alleged incompatibility between Italy's tax system and EU law.

Views of the Council

In March 2025, in its conclusions on 'a tax decluttering and simplification agenda which contributes to the EU's competitiveness', the Council emphasised the need to enhance EU competitiveness by reducing administrative burdens and increasing regulatory certainty, particularly through tax simplification that maintains strong anti-avoidance protections while fostering growth and innovation in the single market. It called for a comprehensive review of EU tax legislation to eliminate outdated rules, streamline reporting requirements, and reduce compliance costs for businesses and tax authorities. The Council invited the Commission to develop an ambitious action plan with clear timelines, involving Member States and stakeholders in this long-term simplification, effort while preserving the effectiveness of tax rules against fraud and aggressive tax planning.

Infringement procedures and CJEU judgments

The European Court of Justice has issued a series of rulings addressing crucial aspects of the ATAD, PSD, IRD, and TMD. A no Court of Justice of the European Union n-exhaustive selection of cases highlights key issues in implementing these directives. No relevant cases interepreting the DRM were identified.

In cases involving the ATAD (C-524/23), the Court has resolved disputes over the transposition of EU directives into national law. For instance, the European Commission brought an action against Belgium for failing to transpose Article 8(7) of ATAD into its national law, which requires Member States to allow a deduction for tax paid by a controlled foreign company from the tax liability of the taxpayer. The Court ruled that Belgium's failure to implement Article 8(7) constitutes a failure to fulfil its obligations under the directive.

The PSD cases (C-135/24, and C-365/16) involved the taxation of parent companies and subsidiaries, with the Court ruling that Belgian legislation that provides for a system of taxation where dividends received by a parent company are first included in the tax base and then deducted, without allowing for a deduction from the amount of an intra-group transfer included in the tax base, is precluded by PSD Article 4(1). Similarly, the Court ruled that PSD Article 4(1)(a) precludes a tax measure that provides for the levy of a tax when a parent company distributes dividends, including those from non-resident subsidiaries, as this would lead to double taxation contrary to the directive.

In the realm of anti-abuse provisions (C-228/24, and joined cases C-504/16 and C-613/16), the Court clarified that the anti-abuse provision in PSD Article 1(2) and 1(3) permits Member States to deny the benefits of the Directive where arrangements are non-genuine and have been put in place to obtain a tax advantage contrary to the object or purpose of the Directive. The Court also ruled that the anti-abuse provision in PSD Article 1(2) in conjunction with Article 5(1) of the PSD and Article 49 TFEU, precludes Member States from refusing withholding tax relief to a non-resident parent company solely because its ultimate shareholders would not have been entitled to that relief if they had received the dividends directly.

The IRD cases (C-397/09, joined cases C-115/16, C-118/16, C-119/16, and C-299/16) involved the exemption of interest and royalties, with the Court ruling that IRD Article 1(1) does not preclude a national tax law provision that incorporates loan interest paid by a company in one Member State to an associated company in another Member State into the basis for assessment of the business tax payable by the former company. The Court also ruled that the exemption provided for in IRD Article 1(1) is restricted to the beneficial owners of the interest, and that national authorities can refuse the exemption in cases of abuse of rights.

Cases on the TMD (joined cases C-662/18 and C-672/18, and C-318/22) involved the taxation of capital gains, with the Court ruling that Directives 90/434/EEC and 2009/133/EC require the same tax treatment for capital gains from exchanged securities and those from transferred securities received in exchange, including tax rates and allowances for the length of time the securities were held. The Court also ruled that national legislation cannot impose conditions, such as a reduction in shareholding or share capital, that are not provided for in the TMD in order to benefit from the directive's tax provisions.

Finally, the Court addressed the scope of the TMD (C-827/21), ruling that EU law does not require national courts to interpret domestic legislation in line with the TMD for purely domestic mergers, as these operations fall outside the directive's scope.

Additionally, several infringement cases are related to the IRD, PSD and ATAD. No infringement cases were found for the DRM and the new FASTER Directive.

For IRD, the Commission launched proceedings in early 2005 against Greece, France, Italy and Portugal (IP/05/39) for failure to notify implementing measures, and separately against the UK over Gibraltar (IP/05/348). These were addressed by letters of formal notice/reasoned opinion.

For the TMD, in 2019 the Commission found that Spain imposed additional conditions on company divisions not required by the directive and referred Spain (INFR(2018)4084) to the Court of Justice in May 2024.

For the PSD, in March 2026 the Commission sent France a letter of formal notice because French law made dividend withholding tax relief conditional on the parent's place of management rather than mere tax residency (INFR(2025)4014). The procedure is ongoing.

For ATAD the Commission referred Belgium to the Court (in April 2023) for not providing the required CFC tax credit. The case is analysed above.

Views of the European Court of Auditors

In 2024, the European Court of Auditors (ECA) published a report entitled 'Combatting harmful tax regimes and corporate tax avoidance'. The report assesses the adequacy of the EU's legal framework to counter harmful tax regimes and corporate tax avoidance framework, including the ATAD and the DRM. Regarding the ATAD, the ECA noted it remained unclear whether the directive would achieve the objectives it had set out, as the Commission's evaluation had been delayed. It also found that differences in national transposition and implementation limited the Commission's ability to assess the directive's effectiveness and the overall impact of EU anti-tax-avoidance measures for combating harmful tax regimes and corporate tax avoidance. The ECA recommended that the Commission develop guidance on the interpretation of EU tax legislation, strengthen monitoring arrangements and establish a framework to measure the effectiveness of anti-tax-avoidance measures.

Regarding the DRM, the ECA found weaknesses in the availability and quality of data on tax dispute resolution procedures, making it difficult to assess whether the directive was achieving its objectives. The ECA recommended that the Commission consider these findings in its future evaluation of the directive and improve monitoring and reporting on dispute resolution outcomes. Overall, the ECA recommended that the Commission clarify the EU legislative framework, including the ATAD and DRM, and strengthen the monitoring and evaluation of results and the impact of the EU measure against harmful tax regimes and corporate tax avoidance.

Views of other EU institutions and advisory bodies

European Economic and Social Committee

In 2025, the European Economic and Social Committee (EESC) adopted an opinion entitled 'Assessing tax reporting obligations in the EU: costs, benefits and effective use of information by tax authorities'. The opinion acknowledged the contribution of EU tax reporting obligations to transparency and the fight against tax avoidance, while noting the growing compliance costs and administrative burdens faced by businesses, particularly SMEs. The EESC identified overlapping reporting requirements, divergent implementation across Member States and inconsistent definitions as factors contributing to legal uncertainty and reduced efficiency of the EU tax framework. It therefore supported further simplification, harmonisation and digitalisation of EU tax rules, alongside systematic competitiveness assessments of future tax legislation.

The EESC further argued that the coherence of EU tax legislation could be improved by reducing duplication between reporting obligations, aligning definitions across directives and promoting a more consistent application of tax rules across Member States. It also highlighted the importance of greater legal certainty for taxpayers through clearer guidance and more effective mechanisms for preventing and resolving tax disputes. At the same time, the EESC stressed that simplification efforts should not undermine the EU's capacity to combat tax avoidance and harmful tax practices.

European Central Bank

In 2026, the European Central Bank (ECB) highlighted the role of tax barriers in hindering the integration of EU capital markets. The ECB noted that withholding tax procedures remain fragmented across Member States, creating administrative burdens, legal uncertainty and additional costs for cross-border investors. While welcoming the adoption of the FASTER Directive as a step towards streamlining withholding tax relief procedures, it argued that differences in national tax systems and cumbersome refund procedures continue to discourage cross-border investment and contribute to market fragmentation. The ECB therefore identified further simplification and harmonisation of tax procedures as important elements in supporting the savings and investment Union and improving the efficiency of EU capital markets.

Expert and stakeholder views

The list of positions below aims to provide an overview of the debate and is not intended to be an exhaustive account of all the different views.

Before the publication of the taxation omnibus, a position paper from Invest Europe, a pan-European organisation representing the private equity industry, called for simplification and harmonisation of the EU's direct tax framework. It stated this has become increasingly complex and fragmented, creating challenges for cross-border investment and hindering the flow of capital to businesses across the single market. It advocated streamlining the ATAD, improving consistency across Member States, reducing administrative burdens, preserving tax neutrality for investment funds, and increasing legal certainty.

Since the proposal was published on 24 June 2026, initial reactions from business and professional organisations suggest the Commission has responded to part of the concerns raised during the consultation. Accountancy Europe, uniting 49 professional organisations from 35 countries that represent a million qualified accountants, auditors and advisors, welcomed the Commission's simplification package. They consider it is moving in the right direction particularly on the exclusion of groups subject to Pillar 2 from the controlled foreign company rules, the automatic adjustment of the interest-limitation threshold to inflation and the removal of the participation thresholds under the PSD and IRD. Additionally, Business Europe, representing 42 national business federations from 36 countries in the EU, European Economic Area and EU neighbourhood, strongly supports the omnibus as a major simplification of the EU corporate tax framework. It welcomes measures to reduce compliance costs, remove withholding taxes on cross-border payments, simplify rules for businesses, and introduce an EU-wide research and development allowance.

Endnotes

Classification

Policy areas: Evaluation of Law and Policy in Practice | Taxation

Committees: Economic and Monetary Affairs (ECON)

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.