Article page checkbox is not checked in page info.

Building a common market for European defence

Building a common market for European defence

Sebastian Clapp and Martin Höflmayr with Falk Vambrie, Members' Research Service

Summary

The European defence industry is highly fragmented, with limited collaborative investment and procurement, divergent national regulations, and protectionist tendencies that undermine efficiency, interoperability and competitiveness. The Letta report makes the case for a concerted effort to advance towards the development of a 'Common Market for the Security and Defence Industry', which focuses on regulatory simplification, pooled procurement, and cross-border industrial integration. While the Draghi report puts its finger on the EU defence sector's fragmentation, under-investment, and external dependencies, it urges coordinated action to strengthen the industrial base, boost joint innovation, and align national efforts through common policies and incentives. According to the White Paper for European Defence, a truly integrated EU defence market would be among the largest globally, strengthening competitiveness, readiness and industrial scale. It would enable firms from the European defence technological and industrial base (EDTIB) to expand across the Union and stimulate cross-border cooperation, mergers and new ventures, increasing the availability of EU-made defence products.

The new Defence Readiness Omnibus aims to remove procedural bottlenecks and facilitate up to €800 billion in defence investment under the Rearm Europe/Readiness 2030 plan, combining streamlined procurement rules, simplified intra-EU transfers, and revised financial instruments. Achieving readiness and autonomy requires predictable joint planning, harmonised standards, and public-private coordination. Without genuine market reform, Europe's rising defence spending risks being absorbed by inefficiencies rather than delivering real capability gains. A functioning common defence market is therefore essential not only for competitiveness, but also for deterrence, resilience and strategic sovereignty in an increasingly volatile geopolitical environment.

The European Parliament advocates a fully integrated internal market for defence to overcome fragmentation, urging regulatory reform, joint procurement, and cross-border industrial cooperation as essential steps towards greater efficiency, competitiveness, and strategic autonomy.

Introduction

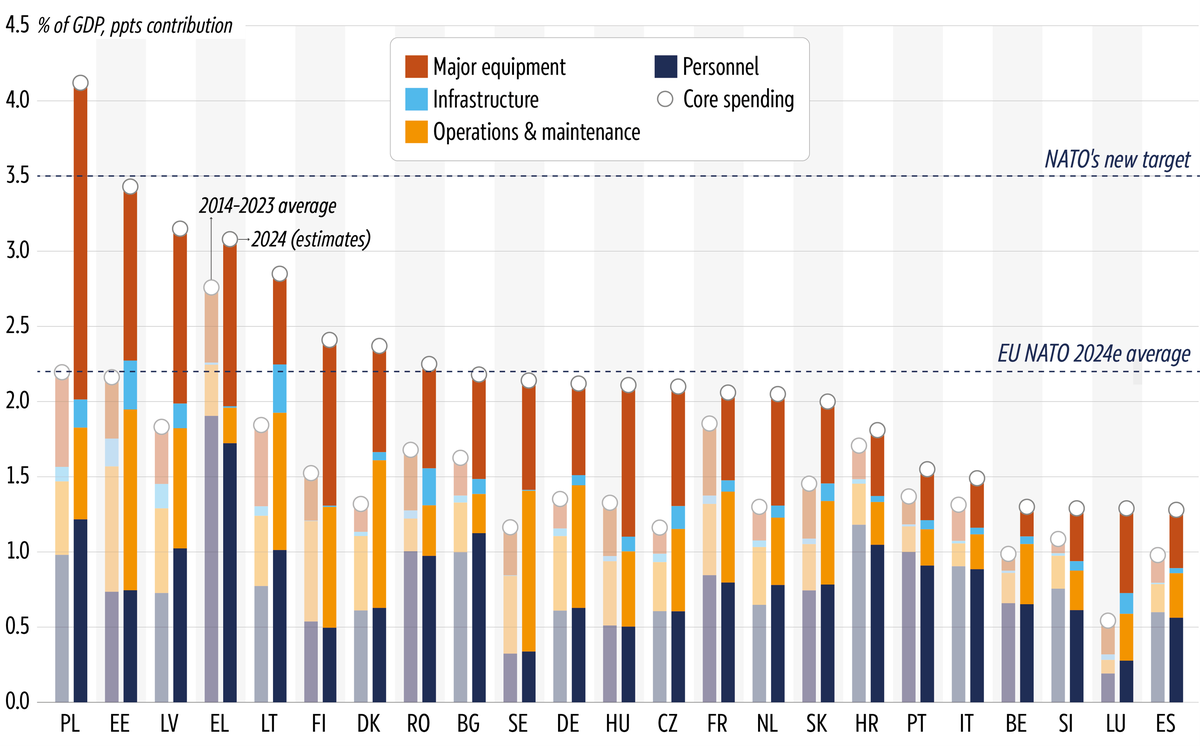

At the 2025 NATO Summit in The Hague, Allies, most of whom are also EU Member States, made a commitment to investing 5 % of GDP annually on defence requirements and defence- and security-related spending by 2035. At least 3.5 % of GDP annually should be allocated to core defence needs and to meeting NATO capability targets. An additional 1.5 % of GDP can go towards protecting critical infrastructure, defending networks, enhancing civil preparedness and resilience, fostering innovation, and strengthening the defence industrial base.

In recent years, NATO members have steadily increased their defence spending, and by 2025 all NATO countries are expected to meet the target of allocating 2 % of GDP to defence. However, European NATO members have a very poor track record of complying with such targets. Therefore, the current European political discourse focuses on urgently increasing collective defence spending. For example, the European Commission proposed activating national escape clauses, which has already been requested by EU Member States, to exclude part of the defence spending increase from the fiscal rules. This arrangement enables Member States to spend more freely on acquiring essential military equipment and developing currently lacking shared European capabilities in the domain of strategic enablers, such as satellites for intelligence, surveillance and reconnaissance (ISR) and secure communication purposes as well as strategic lift capabilities.

For 2025-2027, projections indicate that over half of euro-area defence expenditure will be directed to government consumption – primarily intermediate goods (around 40 %) and personnel (about 15 %) – while close to 40 % will be allocated to investment, a higher share than in recent years.

Source: EPRS, based on NATO data, graphics by Lucille Killmayer, EPRS.

To translate increased defence spending into real defence capability, the unique structure of the European defence industry must be addressed. This sector operates under exceptional conditions: shaped by strategic constraints, dominated by governments as both regulators and customers, and characterised by limited competition. European defence companies remain largely organised within national borders, reflecting fragmented national demand. This market structure, combined with decades of low investment, has left many small-scale national players producing limited volumes. To maximise military power and cost-efficiency, regulators must understand how market power, procurement practices and contractual arrangements shape incentives and pricing – fostering innovation while controlling costs. This way, Europe can ensure its resources support Ukraine effectively against Russian aggression, deter broader threats against the EU, and safeguard shared interests for the future.

Industry structure

| Company | Country | Revenue* | Global ranking |

|---|---|---|---|

| Airbus | European | 12 900 | #13 |

| Leonardo | Italy | 12 401 | #14 |

| Thales | France | 10 593 | #17 |

| Rheinmetall | Germany | 6 145 | #20 |

| Naval Group | France | 4 604 | #27 |

| Saab | Sweden | 4 377 | #29 |

| Safran | France | 4 325 | #30 |

Source: Defense Top 100, 2024. *Revenue from defence in US$ million (2023).

The EDTIB encompasses a mix of large prime contractors, midcaps, and a broad base of small and medium-sized enterprises (SMEs). According to estimates by the European Commission, the sector generated an annual turnover of approximately €70 billion in 2022 and directly employed around 500 000 people. The EDTIB is primarily concentrated in a small number of EU Member States, with France, Germany, Italy, Spain and Sweden hosting the core of industrial capacity. However, a mapping conducted by the Defence Joint Procurement Task Force suggests that the sector is more geographically distributed than headline figures imply: 23 Member States host the prime manufacturers that produce the 46 most urgently required items of defence equipment. Nonetheless, defence industrial capacity remains uneven. In 2024, the largest EU-based defence company by revenue was the transnational Airbus Group, followed closely by Italy's Leonardo, going by defence-related turnover alone. Despite this European presence, the global market is dominated by non-European firms. As of 2024, only 19 of the world's top 100 defence companies were headquartered within the EU, in stark contrast to 48 firms based in the United States. Lockheed Martin, the world's most profitable defence contractor, generated defence revenues of US$71 billion – almost equalling the turnover in 2022 of the entire EU-based defence industry.

Since Russia's invasion of Ukraine, the immediate availability of equipment has emerged as a central concern for EU governments and armed forces. Owing to the larger size of their domestic markets, as in the United States, or to higher levels of defence preparedness, as in South Korea, certain non-European firms were able to sustain greater production capacity and to supply or commit to supplying higher volumes of equipment more rapidly than European firms, which had been constrained by years of contraction and insufficient investment. The United States, in particular, had retained substantial stockpiles and reserves that could be mobilised for partners and for Ukraine at relatively short notice. However, the situation has shifted considerably since the beginning of the full-scale invasion of Ukraine. For instance, the EU has increased its annual ammunition production capacity from 300 000 rounds per annum in 2022 to around 2 million by the end of 2025. According to the Financial Times, Europe's arms factories are 'expanding at three times the rate of peacetime'.

The EDTIB produces a wide spectrum of military equipment and technologies, offering a relatively comprehensive portfolio. This includes military aeronautics, such as combat, transport and mission aircraft, helicopters and engines; land systems, including main battle tanks, armoured vehicles of various categories, logistics and tactical transport, artillery and ammunition across calibres, as well as combat gear; naval assets ranging from submarines to surface ships; space capabilities; missile systems at both tactical and strategic levels; and defence-related electronics, information and communication technologies, cyber capabilities and autonomous platforms, particularly tactical drones. In certain market segments such as MALE UAVs, tactical ballistic missiles and long-range artillery rockets, no European-made solutions are currently available. This absence is the result of decades of under-investment, industrial policy choices by European governments and reliance on the American security guarantee.

For the first time in decades, Europe faces the prospect of potentially having to defend itself without the support of the United States, which has long guaranteed European security. While European militaries are well trained, they especially lack the strategic enablers, command structures, and massed firepower needed for a prolonged, high-intensity conflict. Critical gaps remain in areas such as intelligence, surveillance and reconnaissance, integrated air and missile defence, long-range precision strike, and strategic airlift, all of which are dominated by US capabilities in NATO. At the tactical level, Europe lacks sufficient artillery, missile defence, engineering, electronic warfare, and uncrewed systems to sustain independent operations, despite progress in acquiring advanced aircraft and launching initiatives like the Sky Shield.

The ownership structures of Europe's major defence companies reflect the sector's strategic nature. In many cases, national governments retain blocking or controlling stakes, ensuring alignment with national interests and enabling public oversight. Ownership structures in continental Europe are typically concentrated either in the hands of the state or within family-run enterprises.1 State ownership may act as a barrier to transactional forms of integration, limiting the capacity for cross-border cooperation and consolidation within the defence sector. While merging defence firms could generate economic benefits, notably through economies of scale, such moves may be perceived as strategically problematic, given the implications for national security and sovereign control. Conversely, family-owned firms often follow corporate strategies rooted in national or dynastic priorities, which tend to resist broader European integration. Mechanisms such as 'golden power' provisions in the case of state ownership, or the capacity of dominant family shareholders to block mergers and acquisitions, serve to reinforce this structural rigidity. According to research by the University of Bologna, the cumulative effect is a fragmented and less competitive European defence industrial base, particularly when contrasted with more consolidated markets such as that of the US.

Towards a true common market for defence

The White Paper for European Defence/Readiness 2030 stresses the urgent need to build a common market for defence, arguing that fragmented national markets and dependence on non-EU suppliers undermine Europe's strategic autonomy. With defence spending rising but fragmented, only an integrated EU market can provide the scale, resilience and competitiveness required to strengthen the EDTIB and secure supply chains. A true common market for defence would reduce fragmentation, allow larger production runs, cut costs and improve interoperability. By pooling demand and standardising equipment, it would strengthen supply chains, boost innovation through joint R&D, and enable Europe to scale up production more rapidly in a crisis while reducing reliance on external suppliers. Reflecting this priority, the mandate of the Commissioner for Defence and Space, Andrius Kubilius, places the creation of a true single market for defence products and services at the core of his agenda.

When procuring military equipment, governments must address three fundamental issues:

-

What to buy: Challenges include fragmentation and national protectionism.

-

From whom to buy: Challenges include trust deficits and strategic culture differences, as well as divergent regulatory and certification frameworks.

-

How to contract: Challenges include lack of demand aggregation and joint planning, as well as insufficient budgetary incentives.

The first issue concerns the definition of operational and technical requirements and the make-or-buy dilemma. The second involves choosing between domestic or foreign suppliers, managing protectionist pressures, and overcoming trust and cultural barriers. The third relates to designing contracts and budgetary frameworks that align incentives and contain costs. In Europe, these choices are complicated by persistent fragmentation, regulatory divergence and weak coordination, which undermine efficiency, scale and accountability.

Fragmentation and national protectionism

Europe's defence industry continues to suffer from fragmentation on both the demand and supply sides. On the demand side, the 2022 Coordinated Annual Review on Defence (CARD) by the European Defence Agency (EDA) highlights that only 18 % of investments in defence programmes are conducted collaboratively. The 2024 CARD report underscores that EU Member States' joint investment in collaborative defence R&D remains modest. Collaborative defence procurement also remains limited (see below). As the CARD report underlines, 'cooperation remains the exception rather than the norm', and is typically pursued only when it aligns with national plans, benefits domestic defence industries, or reinforces existing strategic partnerships.

Defence companies are largely structured around national priorities, with demand primarily generated by national governments and directed towards their respective national industries. These industries often maintain close links with their governments, which leads to a proliferation of nationally embedded firms operating within relatively small markets. This arrangement results in insufficient production capacity, which is increasingly inadequate in light of current geopolitical challenges. The lack of collaborative investment in defence has tangible financial implications. According to an EPRS study, enhanced cooperation could generate annual savings of between €18 billion and €57 billion. Beyond economic inefficiency, fragmentation also weakens the EU's interoperability. The EDA has repeatedly pointed out that fragmentation impairs Member States' capacity to carry out joint operations – one of the central objectives of the Strategic Compass and of the common security and defence policy.

On the supply side, the EDTIB remains similarly fragmented, particularly beyond the aeronautics and missile sectors. The European Commission has stressed that this structure significantly limits the industry's ability to strengthen its competitiveness, notably by undermining the pooling of research and development efforts and by restricting the benefits of economies of scale in production. This fragmentation generates costly duplication, complicates logistics, obstructs transnational maintenance cooperation, and hampers interoperability. Thus, defence markets remain heavily nationalised, with Member States frequently favouring domestic suppliers to preserve their strategic autonomy, support national industrial capabilities, and safeguard employment.

Trust deficits and strategic culture differences

Efforts to establish a genuine common market for defence are hindered by trust deficits and a lack of convergence in strategic cultures – defined by then EU High Representative for Foreign Affairs and Security Policy, Josep Borrell, as 'a common way of looking at the world, of defining threats and challenges as the basis for addressing them together'. These differences manifest themselves in day-to-day political decisions, divergent prioritisation of threats, and varying degrees of strategic ambition. While some Member States maintain a traditionally Atlanticist orientation with a strong reliance on NATO, others advocate a more autonomous European defence posture. This lack of alignment often results in a fragmented approach to capability planning, procurement, and threat assessment. The 2003 European security strategy already set out the ambition of fostering a common European strategic culture, yet such a culture remains elusive according to experts.

Infighting over leadership roles in multinational capability development programmes is emblematic of these deeper divides. Disputes frequently arise over which state or consortium leads a given initiative, with national champions often prioritised at the expense of pan-European industrial logic. These tensions are intensified by competition over intellectual property rights (IPR), especially in high-tech and dual-use sectors. The reluctance to share sensitive technologies or manufacturing expertise, even within ostensibly cooperative frameworks, undermines trust and limits the scalability of collaborative projects. For instance, at the Paris Air Show in June 2025 Airbus and France's Dassault Aviation openly clashed over governance, workshare distribution and intellectual property control in the Future Combat Air System (FCAS) next‑generation fighter programme, threatening delays unless the dispute is resolved politically. According to Politico , Germany's growing frustration with France over the FCAS has led Berlin to consider alternatives, including cooperation with Saab in Sweden or BAE Systems in the UK, unless a compromise is reached by the end of the year. While France insists it remains committed to FCAS, political uncertainty in Paris and the industrial deadlock between Dassault, Airbus and Indra have increased pressure on Berlin to prepare fallback options.

Divergent regulatory and certification frameworks

Different national standards, export controls, and certification processes constitute another major impediment, increasing compliance costs for industry and limiting cross-border cooperation. Defence procurement legislation is a highly fragmented area, with defence procurement contracts subject to a vast array of different national procurement regimes in EU Member States. These different regimes have discouraged cross-border competition and, as a result, experts find that there has never been a 'genuine pan-European defence procurement market, but rather ... [27 markets] fenced off with regulatory barriers to entry aimed at protecting national defence industries'. Indeed, Article 346 of the Treaty on the Functioning of the European Union (TFEU), which allows EU Member States to derogate from EU rules and adopt extraordinary measures in the trade and production of munitions, arms and war material, has been seen by many Member States as giving them carte blanche to circumvent EU procurement rules.

The fragmentation of the European defence market, coupled with divergent national approaches, has created persistent challenges for the defence industry as a whole. Varying national licensing regimes have introduced complex and burdensome administrative requirements, which in turn have undermined the reliability of supply chains within the EU.

The 2009 Transfer Directive seeks to ease intra-EU transfers of defence equipment by streamlining licensing while preserving Member States' control over national security. It introduced a modified licensing framework that distinguished between general, global and individual licences while streamlining their application. It encourages EU Member States to substitute individual licences with general licences wherever feasible, in order to facilitate smoother transfers within the Union. General licences refer to standardised authorisations granted by national authorities that allow defence companies to transfer specific categories of military equipment or components within the EU without having to apply for an individual licence for each transfer. Although individual licences are still possible, they are meant to be limited.

In 2009, the Directive on defence and sensitive security procurement, which sets out European rules for the procurement of munitions, arms and war material, entered into force. As a 2016 Commission evaluation report notes, most procurement contracts, especially for 'high-value, strategic, complex defence systems', are still awarded without an EU-wide tender; Member States continue to invoke Article 346 TFEU to circumvent procurement rules. The evaluation notes that, while 'the overall text of the Directive is fit for purpose...there is a strong need to focus on its effective implementation, in order to improve its effectiveness and in turn, its efficiency'. This finding is also backed up by an EPRS study. The 2016 evaluation of the Transfer Directive found that, while the Directive simplified procedures for transferring defence products within the EU, its impact was limited by divergent national practices and low uptake of general licences. Certification of defence firms was under-used, and the internal market remained fragmented.

Legislation on export controls is equally fragmented, with each EU Member State being responsible for its own arms export controls. However, all European arms exports are governed by a combination of legal instruments, namely the EU Common Position adopted by the Council, the Arms Trade Treaty, which all EU Member States are party to, and arms embargoes imposed either by the EU or the UN. The EU Common Position requires Member States to assess export licences against eight shared criteria, including considerations such as respect for human rights and the preservation of regional peace and stability. While these criteria provide a common foundation, implementation is decentralised: each Member State retains discretion over licensing procedures and how it interprets the Common Position. The Common Position was amended in 2025 to strengthen controls and accountability over international arms trade.

Additionally, Regulation (EU) 2021/821 establishes a comprehensive EU-wide regime governing the export, brokering, technical assistance, transit and transfer of dual‑use items – which are goods, software or technology that can serve both civilian and military purposes – drawing on internationally agreed control lists (such as the Wassenaar Arrangement) and imposing authorisation requirements (general, global, individual, and for large-scale projects), with stringent provisions on end-use, record‑keeping, and coordination among Member States' authorities.

Although these frameworks provide a degree of convergence, the absence of a harmonised EU export control system continues to generate obstacles for the functioning of a defence single market. Defence production today relies heavily on integrated cross-border supply chains, with components sourced from multiple Member States. If one Member State denies an export licence for a component manufactured on its territory, this can block the export of an entire system assembled in another Member State, creating uncertainty for industry and undermining the predictability of supply chains. The European Commission has recognised this problem, which was one of the drivers behind Directive 2009/43/EC on the intra-EU transfer of defence-related products (see above). However, as noted above, implementation of the directive is lacking.

Lack of demand aggregation and joint planning

In a highly specific market where national governments are the sole customers, EU Member States continue to fall short in coordinating, pooling and aligning their defence planning and procurement, despite the availability of various European mechanisms designed to facilitate such collaboration. As a result, demand remains largely fragmented along national lines, with investment decisions predominantly shaped by domestic agendas and national planning cycles, often at the expense of broader strategic coherence or cost-efficiency.

EDA data from 2020 show that Member States spent only €7.9 billion on collaborative equipment procurement, which is 18 % of total defence equipment procurement – far below the 35 % benchmark agreed within the EDA framework in 2007 and the related Permanent Structured Cooperation (PESCO) commitment. More up-to-date data are unavailable due to persistent gaps in data sharing by Member States. The 2024 CARD report notes that the pressing need to address capability shortfalls rapidly has prompted a rise in national off-the-shelf acquisitions, which, while expedient, have contributed to a temporary decline in collaborative procurement efforts. These are often viewed as more complex and time-intensive. To counter this trend, the European Defence Industry Reinforcement through Common Procurement Act (EDIRPA) was introduced to encourage joint procurement among Member States, yet collaborative procurement remains far below the EU goal – as enshrined in the European defence industrial strategy (EDIS) – that, by 2030, Member States should procure 40 % of defence equipment in a collaborative manner.

In terms of planning, rather than having one integrated tool for defence planning, the EU has established several overlapping processes. Since 2008, the EDA has used capability development plans (CDPs) to identify future capability needs and recommend how European forces can meet them. The latest CDP review in 2023 outlined 14 priorities across five military domains (land, air, maritime, space, cyber) and eight priorities under strategic enablers and force multipliers. The EU also launched PESCO in 2017, which introduced 20 legally binding commitments and initiated 83 collaborative projects, 75 of which are still ongoing. The CARD by the EDA provides an EU-level overview of defence landscapes and identifies collaborative opportunities.

Further initiatives include the European Defence Fund (EDF), launched in 2017 with an €8 billion budget for 2021-2027, which incentivises joint defence research, innovation, and capability development. The 2022 Strategic Compass called for further adaptation of EU defence planning and annual defence ministerial meetings on EU initiatives. Most recently, the Defence Industrial Readiness Board, being set up under the European defence industry programme (EDIP), aims to coordinate procurement plans, align industrial capacities with strategic priorities, and set common production objectives, particularly for critical capabilities.

However, EU defence planning remains difficult and fragmented. Experts note that 'defence planning remains stuck at the national, rather than at the European or even Atlantic level', primarily due to a lack of political will. This is particularly problematic as coordinated action on strategic enablers – often too expensive for smaller Member States alone – is essential to reduce reliance on US assistance, whose future support and its size cannot be taken for granted.

Insufficient budgetary incentives

Despite significant steps taken by the European Commission since Russia's 2022 invasion of Ukraine to incentivise joint procurement, budgetary support and financial incentives remain insufficient to fully address Member States' reluctance to collaborate. EDIRPA allocated €300 million to incentivise Member States to jointly procure urgent and critical defence capabilities. The forthcoming EDIP, still under negotiation, is set to provide €1.5 billion for 2025-2027 to enhance the competitiveness and resilience of the European defence industry and support joint procurement.

To address this gap, in March 2025, Commission President Ursula von der Leyen unveiled the ReArm Europe Plan/Readiness 2030, a strategic proposal aimed at enabling up to €800 billion in defence investment and firmly anchoring Europe's shift towards joint responsibility for its own security. The plan reflects Europe's entry into an 'era of rearmament' and focuses on speeding up and scaling up collective defence spending through coordinated financial mechanisms.

The plan is structured around five key pillars, each designed to strengthen Europe-wide collaboration in defence spending and procurement:

-

Security Action for Europe (SAFE): This will provide up to €150 billion in EU-backed long-term loans for Member States to finance joint procurement of defence equipment from European industry, thereby improving interoperability and fostering deeper integration; it is also open to partners like Ukraine and EFTA/EEA countries. The JURI committee has asked European Parliament President Roberta Metsola to challenge the legal basis of SAFE at the Court of Justice of the EU, as the Commission bypassed Parliament in the legislative process.

-

Boosting national defence funding: This will allow Member States more fiscal flexibility under EU rules to increase defence spending and reach the new NATO target, to free up national funds for investments.

-

Making EU instruments more flexible: This will enable quicker reallocation of existing EU cohesion and regional funds to defence-related projects that also stimulate innovation and local economies.

-

European Investment Bank (EIB) support: The EIB's role in financing defence and security projects will be expanded, complementing public funds and building investor confidence.

-

Mobilising private capital: Private investment will be leveraged through the savings and investments union to ensure sustainable financing across the defence sector.

Together, these pillars aim to make joint procurement financially attractive and viable, enhance strategic coordination, and foster a more integrated European defence market – encouraging Member States to align spending plans and invest collectively rather than individually.

Owner, regulator, customer: Structural specificities of the defence market

Public procurement in the defence industry

To make aggregated procurement effective, contracting models must also be chosen carefully. Defence contracts largely fall into three categories, each with distinct advantages and drawbacks:

- cost-plus contracts reimburse all actual costs plus a profit margin,

- fixed-price contracts specify a lump sum and shift cost risk to the contractor,

- target-cost contracts strike a balance by sharing risks and rewards between government and contractor.

All three approaches are prone to inefficiencies due to information asymmetries, moral hazard, and strategic behaviour during contract negotiation and execution.

The persistence of fragmentation and national prerogatives in European defence markets cannot be understood solely through the lens of legal derogations or institutional inertia. Instead, it reflects a more fundamental structural reality: defence is not a conventional economic sector, but one shaped by the state's unique triple role as owner, regulator, and primary customer. As a public good, defence is provided by states, and coordinated – rather than centralised – at EU or NATO level. The defence industry is unique because it produces sensitive products (such as armaments, strategic enablers, and dual-use goods) subject to national export controls, which the Council is aiming to harmonise. Due to the strategic nature of defence products, procurement contracts are often subject to tailored procedures that may not adhere strictly to the standard principles of open competition applied in other sectors. As a result, the market exhibits both monopsonistic (on the demand side) and oligopolistic (on the supply side) characteristics.

This mutually constrained relationship between seller and buyer is what Wang & Miguel (2013) call a 'sole-buyer-and-sole-seller case', where the government's limited supplier base reduces its bargaining power, while contractors are similarly constrained by their reliance on government contracts. If a defence company refuses to accept a fixed-price contract, the government may face significant challenges in identifying a suitable replacement. This limited supplier base can constrain the government's bargaining power. At the same time, defence contractors are also constrained, because their primary/only customer is the government. This means they are highly dependent on (domestic) government contracts for survival. If they refuse to accept certain contractual conditions, they risk losing future procurement opportunities.

Public procurement typically relies on fixed-price or cost-plus contracts, each influencing project costs and taxpayer burden, potential for innovation, and profitability. On the one hand, fixed-price contracts set the terms of a project, outline the seller's obligations exactly, and establish the final price of goods or services. Any exceeding costs are the responsibility of the seller. On the other hand, under cost-plus contracts, the buyer reimburses the seller for all the actual costs incurred, plus an additional amount for managing the project. The profit usually equals a percentage of the contract's full price. To maintain oversight, the seller is generally required to share detailed cost and pricing data with their customer.

Given the considerable uncertainty in the defence investment landscape, cost-plus contracts are more desirable from the seller's (industry) perspective, as they guarantee profitability through a fixed fee or percentage revenue above project costs. This is particularly important. To mobilise private capital effectively under such risk, governments can offset part of the burden through cost-plus contracts, mark-ups in fixed-price contracts (acting as a risk premium), or by taking on the role of major shareholder. As a result, cost-plus contracts may also support innovation and the development of cutting-edge technologies that would otherwise be too risky to finance. However, the customer (government) may prefer fixed-price contracts, as these ensure predictability of expenses and incentivise the seller to rigorously control costs, impeding artificial cost inflation and windfall profits. They can be particularly effective at facilitating fair pricing when buying commercial off-the-shelf products where costs per unit tend to be comparatively low and/or well known, but may be less applicable for developing innovative and complex systems because of the unpredictability involved in the process. Wang & Miguel propose a budget-based cost-plus scheme that aligns government and industry incentives by ensuring transparent cost disclosure, curbing opportunistic behaviour, and fostering both fairness and innovation through balanced risk-sharing.

Furthermore, industrial policy can encourage investment in the defence sector. At the moment, the European defence industry is fragmented and supply-constrained. Governments face limited defence industrial production capacity due to decades of under-investment, whereas the perceived threat level has dramatically increased since the start of the Russian war on Ukraine, pushing European countries (as member states of the EU and NATO) to urgently rearm to ensure sufficient defence-readiness and deterrence. This seasonal demand contingent on external threat runs contrary to the long-term and aggregated demand signals required by defence companies to scale up and maintain high production capacity. It also conflicts with the long timelines needed to develop cutting-edge military technologies and implement large-scale projects, such as sixth generation fighter jets, or space capabilities.

Defence omnibus

The Draghi report on European competitiveness exposes deep structural flaws in the EU's defence sector – ranging from fragmented governance and external dependencies to under-investment and barriers for SMEs – and stresses that Member States' lack of coordination has left spending inefficient and inadequate. To address these weaknesses, it proposes a comprehensive strategy centred on strengthening the EDTIB, fostering joint investment and innovation, and aligning national efforts through policies such as the EDIS and EDIP, aggregated demand, and incentives for EU-made capabilities. In a similar vein, the Letta report highlights the growing urgency of creating an EU-wide market for defence equipment. Member States now purchase up to four times more equipment than a decade ago, often from non-EU suppliers, while no national market alone is large enough to scale up the EDTIB. Ensuring reliance on the EDTIB and securing European supply chains, particularly in crises, requires guaranteed access to systems, components and spare parts through a strong security of supply framework. According to the White Paper on European Defence, a truly integrated EU defence market would be among the largest globally, strengthening competitiveness, readiness and industrial scale. It would enable EDTIB firms to expand across the Union and stimulate cross-border cooperation, mergers and new ventures, increasing the availability of EU-made defence products. Achieving this depends on regulatory simplification in procurement, intra-EU transfers and certification, as well as reassessing the impact of broader EU policies on the defence sector.

The Commission therefore tabled the Defence Readiness Omnibus simplification proposal in June 2025. It aims to facilitate up to €800 billion in defence investment over the next four years under the ReArm Europe Plan/Readiness 2030, allowing Member States and industry to react more rapidly and effectively to escalating security challenges. The Commission argues that the EDTIB is a unique sector, focused not on economic output alone but on meeting the operational needs of Member States' armed forces with high-performance capabilities delivered at speed and scale. To this end, EU regulation must be simplified to facilitate investment, procurement and research while maintaining environmental and social standards. This includes adapting procedures across sectors to accelerate industrial production and ensure credible deterrence. The Defence Readiness Omnibus acknowledges that the EU's current regulatory framework, designed for peacetime, must be adapted to support the rapid development and deployment of defence capabilities.

The package comprises a Commission communication along with legislative and non-legislative proposals that address both defence-specific and wider regulatory areas, aiming to eliminate persistent bottlenecks in procurement, permitting, reporting and cross-border coordination. It introduces simplified administrative procedures for the EDF, faster grant delivery and greater implementation predictability, drawing on stakeholder feedback and the fund's interim evaluation. In the field of procurement, it proposes streamlined processes for contracting authorities and industry, including incentives for joint procurement by at least three Member States, simplified off-the-shelf purchases to replenish stocks, enhanced flexibility in framework agreements, and higher thresholds for supply and service contracts under the Defence Procurement Directive. Intra-EU transfers of defence products, often delayed by up to a year, are to be accelerated through eased authorisation processes – particularly vital for EDF-supported projects.

Beyond the defence-specific framework, the Omnibus advances a fast-track permitting regime for defence-related infrastructure with a two-month approval window and a single contact point in each Member State. It also clarifies the application of derogations in environmental and chemicals legislation for projects serving overriding public interests, enabling Member States to support investments involving critical substances. In the financial domain, the package adjusts InvestEU eligibility and provides guidance to align defence readiness with sustainable finance principles, while clarifying that only internationally prohibited weapons should be excluded from sustainability indices under the benchmark regulation, offering legal certainty and supporting the mobilisation of €800 billion in investment.

According to a regulatory expert, the Omnibus proposal marks a strategic shift in the EU's application of competition and state aid rules to defence, signalling a more flexible stance on joint purchasing, production and consolidation that strengthens EU defence capacity. While pragmatic interpretations of Article 346 TFEU will apply, companies must still ensure compliance with core competition principles and are advised to consult the Commission where doubts arise, as abuse of this flexibility will not be tolerated. Another analyst notes that the Defence Readiness Omnibus is a significant regulatory shift that aims to make defence investment more accessible and compatible with the EU's sustainable finance framework, potentially unlocking greater private capital for the European defence sector. While recognising the political importance of aligning defence policy with financial sustainability goals, the analyst notes that asset managers will need to reassess exclusion policies and perform enhanced due diligence – particularly on export controls and controversial weapons – to ensure compliance, given the EU's new guidance discouraging broad-based exclusions of the defence sector. Another regulatory expert sees the Defence Readiness Omnibus as a pivotal reform package aimed at cutting significant regulatory red tape, with the potential to strengthen Europe's defence industrial base, but its impact hinges on how swiftly and effectively the proposals are implemented within the next few years.

Conclusion

Achieving European defence readiness and effective deterrence vis-à-vis Russia relies not only on increased financial input, but also on the ability to translate spending into a scaled-up defence industry and improved military capabilities. Given the fragmented and supply-constrained nature of the European defence industry, shaped by monopsonistic and oligopolistic dynamics, this process depends on the provision of aggregated and predictable demand signals, the use of appropriate contractual arrangements, and effective strategic and procurement coordination. Contract types, such as fixed-price, cost-plus, or budget-based cost-plus schemes, play a critical role in shaping incentives, fostering innovation, and ensuring cost control. The dual role of governments as both customer and shareholder contributes to the sector's strategic orientation and requires democratic oversight. Taken together, these structural features influence how effectively spending increases will in fact strengthen Europe's military production and warfighting capacity.

European Parliament position

The European Parliament strongly supports the creation of a genuine internal market for defence, arguing that fragmentation in the EU's defence industrial landscape continues to hinder efficiency, drive up costs, and delay capability development. It calls for full implementation and, where necessary, revision of key directives on defence procurement and intra-EU transfers, alongside a clearer interpretation of Article 346 TFEU to limit its misuse for protectionist ends.

Parliament supports the calls under the EDIS and the proposed EDIP to strengthen joint procurement, reduce duplication, and establish pan-European value chains. It calls for harmonised regulation, improved oversight, and the removal of legal and structural barriers to cross-border industrial cooperation, emphasising that a functioning single market for defence is essential to competitiveness, readiness, and strategic autonomy. Parliament is working on an own-initiative report (2025/2143(INI)) entitled 'Tackling barriers to the single market for defence ' (Rapporteur: Tobias Cremer, S&D, Germany).

Main references

- French defence procurement agency, International Defence Companies, Notebook, 2025 edition.

- Harley, K., The Case for Markets in Defence: Driving efficiency and effectiveness in military spending, Institute of Economic Affairs, 2023.

- Centrone, M. and Fernandes, M., Improving the quality of European defence spending, EPRS, European Parliament, 2025.

Endnotes

Classification

Policy areas: Security and Defence

Committees: Security and Defence (SEDE), Industry, Research and Energy (ITRE)

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.