Article page checkbox is not checked in page info.

Confiscation of immobilised Russian sovereign assets: State of play, arguments and scenarios

Confiscation of immobilised Russian sovereign assets State of play, arguments and scenarios

Anna Caprile and Tim Peters with Ana Luisa Melo Almeida, Members' Research Service

Summary

One of the first, and boldest, measures taken by Western countries as a response to Russia's full-scale invasion of Ukraine in February 2022 was the immobilisation of the Russian central bank assets held under their jurisdictions, the value of which could be around €300 billion worldwide, according to recent estimations.

As the war is well into its fourth year, the debate on how to use the immobilised assets to sustain Ukraine's reconstruction efforts – a cost estimated at US$524 billion – has evolved. A growing number of international legal experts and prominent political figures have defended the lawfulness of confiscating Russian central bank assets to sustain Ukraine, both for financing reconstruction efforts and military expenses, despite these assets being protected by state immunity. However, opinions among legal scholars differ significantly, as do the positions of the governments in whose countries these assets are held.

G7 countries reached an agreement in October 2024 on using the extraordinary revenues generated by those assets to service and repay a US$50 billion G7 loan to Ukraine, while the complex debate on the legality and related risks on the use of the principal capital continues. In the absence of a clear precedent or an uncontested legal basis, political considerations, such as US policy shifts, and calculations over the economic and financial risks incurred will play a decisive role in this debate. Notably, this subject was on the agenda, for the first time, of the informal meeting of EU foreign ministers in Copenhagen on 29-30 August 2025.

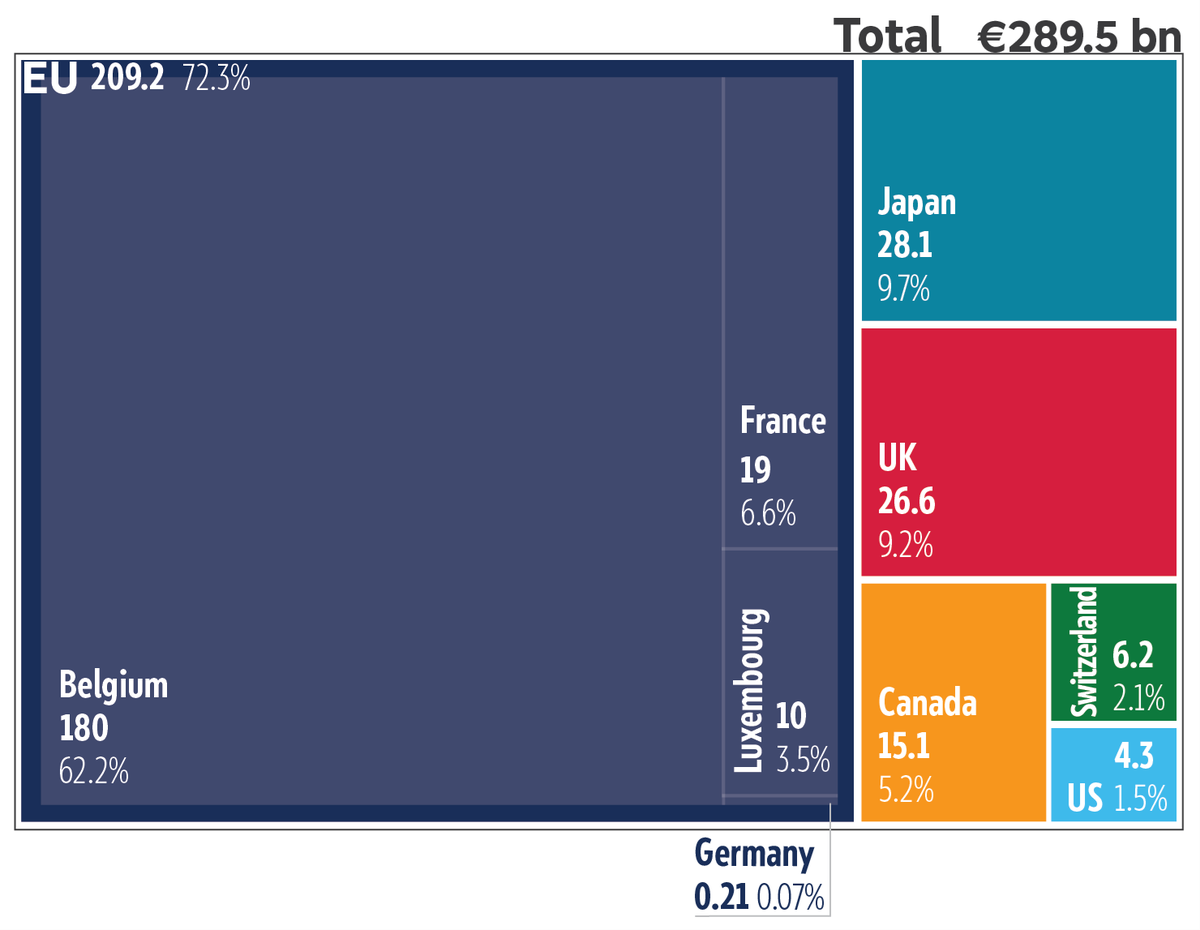

Where are the immobilised Russian central bank assets?

Source: EPRS, data from PISM, Swiss Federal Government; graphic by Nadejda Kresnichka-Nikolchova, EPRS. For Luxembourg, where estimations vary from 'several billion euros to around €20 billion', the authors opted for a conservative figure (€10 billion).

Within days of Russia having launched its full-scale aggression against Ukraine on 24 February 2022, the EU included in its third package of sanctions the prohibition of any transaction related to the management of reserves and assets of the Central Bank of Russia (CBR), thus immobilising ('freezing') approximately €210 billion worth of assets held under EU Member States' jurisdictions. The non-EU G7 countries (the US, the UK, Canada and Japan), together with Australia and Switzerland, adopted similar measures.

The total worth of Russian sovereign assets immobilised by the EU and the other G7 countries was estimated in February 2024 at €260 billion , and the value of the immobilised assets worldwide, including non-G7 countries, could be nearly €300 billion, according to recent calculations (Figure 1).

Determining the exact value of assets under each jurisdiction is difficult1 due to a lack of consistent official information, a transparency problem which many experts have pointed out. Most assets held in the EU are managed by Euroclear, a large international securities depository and clearing house registered in Belgium, and therefore subject to Belgian and EU law. A less significant part is held in a similar organisation, Clearstream, registered in Luxembourg.

When first immobilised, most of the Russian state assets were debt securities in the form of government bonds, but a large portion – up to 90 % – have matured into cash by now. In the absence of instructions by the lawful owner of the deposits, since the CBR is under sanctions, this cash is held in low-risk accounts. For example, in the case of Euroclear, this cash is, by law, deposited into Belgian central bank investments, which offer the lowest risk-free rate of return available.

As the war is well into its fourth year, the debate on how to use those immobilised assets to sustain Ukraine's reconstruction efforts – a cost estimated at US$524 billion as of December 2024 by the Ukrainian government, the World Bank Group, the European Commission and the UN – has evolved. A growing number of international legal experts and prominent political figures have defended the lawfulness of confiscating Russian central bank assets to sustain Ukraine, both for financing reconstruction efforts and military expenses, despite those assets being protected by state immunity under international customary law.

So far, G7 countries have only reached an agreement on the use of the extraordinary revenues generated by the assets to service and repay a US$50 billion loan to Ukraine from G7 countries, while the complex debate on the legality and related risks on the use of the principal capital continues. As the US financial support for Ukraine dwindles under the Trump administration, while its position vis-à-vis Russia seems to be shifting, the political pressure to take a more decisive stand has increased among EU Member States.

The G7 agreement on the use of extraordinary revenues

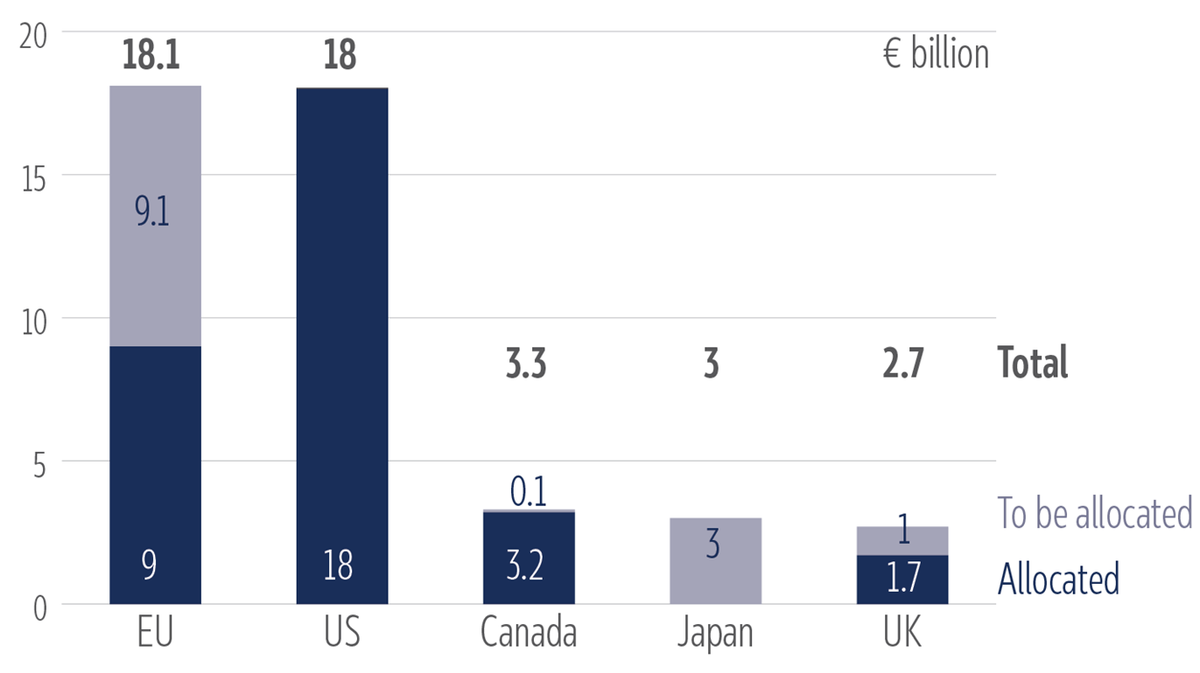

In October 2024, the G7 countries reached an agreement on how to provide US$50 billion (approximately €45 billion) in extraordinary revenue acceleration (ERA) loans to Ukraine. The loans will be serviced and repaid by future flows of extraordinary revenues stemming from the immobilisation of Russian sovereign assets, 'in line with G7 countries' respective legal systems and international law', and 'will enter into force no later than 30 June 2025'.

As detailed in the relevant Council Regulation, 'extraordinary revenues' are the unexpected revenues generated by the 'extraordinary and unexpected accumulation of cash balances on the balance sheets of central securities depositories' where the immobilised assets are deposited, 'due to the immobilisation of assets and reserves of the Central Bank of Russia'. These extraordinary revenues, the rationale goes, 'do not have to be made available to the Central Bank of Russia under applicable rules, even after the discontinuation of the transaction prohibition. Thus, they do not constitute sovereign assets' and, therefore, 'the rules protecting sovereign assets are not applicable to these revenues'.

A few days before the final G7 agreement, the EU had already greenlighted its part of the deal: an extraordinary macro-financial assistance (MFA) loan of €18.1 billion to Ukraine, and the setting up of the Ukraine Loan Cooperation Mechanism , in charge of channelling the extraordinary revenues to Ukraine to repay the eligible G7 ERA loans, including the EU's MFA loan. On 10 December 2024, the US disbursed its share in full, transferring a US$20 billion loan into a financial fund recently established by the World Bank, for further allocation to eligible uses in Ukraine through approved projects . The G7 agreement furthermore contains loans from Canada ( CA$5 billion ), Japan ( JPY471.9 billion ) and the UK (£2.26 billion ), and specifies that the assets 'will remain immobilised until Russia ceases its war of aggression and pays for the damage caused to Ukraine by its war'.

So far, the EU has allocated €9 billion of the committed loan, while allocations by the other G7 countries can be seen in Figure 2. It is important to highlight that not all allocated funds have already been disbursed to the Ukrainian government since some countries, such as the US and Canada, direct a substantial part of their allocations through World Bank or IMF intermediary funds.

The debate: Confiscation, status quo or an alternative way?

The arguments for and against confiscation of immobilised Russian sovereign assets pertain to three different categories: legal basis, economic-financial implications and political considerations.

| For | Against | |

|---|---|---|

| Legal basis 2 | The doctrine of collective state countermeasures, based on Articles 49-54 of Articles on the Responsibility of States for Internationally Wrongful Acts (Annex to UN General Assembly Resolution 56/83 of 12 December 2001, as amended) allows 'states lawfully to carry out measures – that would otherwise be illegal – against a state that has violated fundamental rules of international law, in order to induce it to cease its unlawful conduct or to comply with its obligation to compensate states injured by this conduct'. |

- Customary international law provides strong protection of sovereign assets, partly codified in the 2004 UN Convention on Jurisdictional Immunities of States and their Property (not yet in force). Sovereign immunity is also codified in national legislation. - Countermeasures should be temporary and reversible, two conditions not fulfilled by expropriation. - Countermeasures applied by other than the injured state (collective countermeasures) are not sustained in international law. - Confiscation would, in any case, request a change in national legislation for most of the jurisdictions affected.3 (Source) |

| Collective self-defence under Article 51 of the UN Charter, which recognises 'the inherent right of individual or collective self-defence if an armed attack occurs against a Member of the United Nations, until the Security Council has taken measures necessary to maintain international peace and security'. |

- Self-defence might not be applicable to non-forcible measures such as confiscation. - Joint invocation of self-defence might imply that the countries involved consider themselves to be at war with Russia. (Source) |

|

|

The UN Uniting for Peace procedure allows the General Assembly to take over the Security Council's competence when it fails in its duty to maintain peace and security. (Source) |

- Unlikely to receive the necessary support (two-thirds majority of UN Members). (Source) |

|

| Financial risks |

- The Kyiv School of Economics (KSE) Institute found no evidence that the immobilisation of Russian reserves triggered a structural shift away from G7 currencies. - The euro's share in global reserves has remained stable at 20 %, broadly unchanged since the start of Russia's full-scale invasion. - In the short to medium term, there are few realistic alternatives to G7 currencies due to political, economic, and market constraints. (Source) |

- The European Central Bank (ECB) warned that breaches in third countries' asset protection could undermine the euro's credibility, weaken confidence in international monetary arrangements, and discourage central banks from holding euro-denominated assets. - Financial risks will be significantly higher if G7 countries act individually and not simultaneously. |

|

- Confiscation could have positive effects on sovereign debt markets, reducing the need to issue about €230 billion in new debt to finance Ukraine's defence and reconstruction, and easing pressure on bond yields. - The ECB has effective tools such as the Transmission Protection Instrument and Outright Monetary Transactions to manage risks and stabilise debt markets. |

- Investor confidence in European sovereign debt could fall if major holders (e.g. China and Saudi Arabia) reduce their exposure, raising borrowing costs for euro-area governments. - The Belgian government, in particular, has warned before about possible consequences for Euroclear. Currently, Euroclear invests state assets with the Belgian central bank. - The threat of a Russian response, either in the form of litigation in courts or of retaliation against Western companies still operating in Russia. |

|

| Political factors |

- Using CBR assets now for rearming and rebuilding Ukraine will alleviate the financial burden on EU taxpayers, which is especially relevant after NATO countries committed to paying for US arms deliveries to Ukraine, while increasing their own core defence expenses to 3.5 % of GDP annually by 2035. - Confiscation or temporary transfer to a segregated escrow fund would guarantee long-term reliability of EU support to Ukraine and eliminate the need for unanimous renewal of EU sanctions every six months. |

- Confiscating the assets now would deprive the West of a substantial bargaining chip in eventual negotiations; it should rather be used as a threat in case Moscow violates an eventual ceasefire. - Confiscation of state property will create a dangerous precedent in international law, which would allow the use of expropriation as a coercive measure in the future (or retroactively), opening a potential Pandora's box. |

Source: EPRS, author's elaboration.

Possible alternative scenarios

Between the highly controversial direct confiscation of the Russian assets and the status quo (i.e. the current G7 framework), alternative scenarios are being contemplated. The table below is an adaptation of one elaborated by the Polish Institute of International Affairs (PISM), describing scenarios other than direct confiscation, from the most to the least controversial.

| Scenario | Key points and challenges |

|---|---|

| Payment of damages awarded by an international claims commission |

– The need for a commission to be set up by as many states as possible, to give it legitimacy (either under the auspices of the UN General Assembly according to the 'Uniting for Peace' resolution, or under the auspices of the Council of Europe). – Creation of a fund from which the commission would allocate resources. – Disbursement of funds requiring decisions ordering the payment of damages, probably faster than judgments of international courts but slower than administrative confiscation. – Need to adopt regulations enabling the transfer of funds to the commission/fund without the involvement of national courts, or to include such a solution in the treaty establishing the commission. - Until this scenario is implemented, the immobilisation of assets depends on EU sanctions renewal every six months. |

| Payment of damages awarded by international courts and tribunals |

- Limited possibilities of obtaining reparation awards outside of a few tribunals (ICJ and ECHR). - Payment would require judgments awarding damages, which could take several years. - Procedural issues specific to each tribunal. - The need to adopt rules allowing the transfer of funds on the basis of an international tribunal judgment without the involvement of national courts. - Until this scenario is implemented, the immobilisation of assets depends on EU sanctions renewal every six months. |

| Use of CBR assets as collateral for loans or bonds for Ukraine's support |

- A measurable reduction in risk for lenders or debt buyers is only possible if there is a real prospect of satisfying claims on the collateral. - Requires the transfer of assets to government trust accounts in individual countries, i.e. central banks or the European Central Bank. - Requires a change in the national laws of most G7 members, as well as a willingness to waive the protection afforded to CBR assets by sovereign immunity, in the same way that direct confiscation would require. |

| CBR assets as collateral for reparation payments under a future peace agreement |

- Requires setting a time limit within which it can be conclusively determined that Russia has refused to pay reparations, after which the confiscation of CBR assets should follow. - In the event of a clear refusal by Russia to pay reparations or the lapse of a sufficiently long period of time, there would be a need to reopen the discussion on how to use the CBR assets anew. - Essentially, it represents a continuation of the status quo, not directly threatening state immunity norms and therefore eliminating legal and financial risks. - Unless the assets are transferred to a separate government or a multilateral trust account (see below), this scenario is permanently subject to EU sanctions renewal every six months. |

| Transfer of CBR assets into separated escrow accounts |

- Transfer of CBR assets, in particular cash, into clean escrow accounts for trust management, without changing the ownership, for protection and professional reinvestment. - This scenario can be seen as a temporary step towards confiscation or any of the scenarios above, but can also become a scenario in its own right since it addresses several key points (no need for renewal of EU sanctions, protection of assets and reasonable profitability ensured, decision on confiscation or alternative scenarios can be postponed). - Scenario debated during the informal meeting of EU foreign ministers, 29-30 August 2025. - Euroclear management regards this move as being equivalent to 'expropriation' and points to risks liability. - Critics warn that EU taxpayers may have to cover losses from any unproductive investments. |

Source: Adaptation by EPRS authors of PISM table (PISM report, p. 65).

Positions of the European Parliament and countries involved

In its resolution of 19 September 2024, the European Parliament welcomed the G7 decision and repeated its calls for the EU 'to take the work forward, together with like-minded partners, by adapting sanctions legislation as necessary and by establishing a sound legal regime for the confiscation of Russian state-owned assets frozen by the EU'.

In its 12 March 2025 resolution on 'Continuing the unwavering EU support for Ukraine, after three years of Russia's war of aggression', Parliament 'reiterates its firm conviction that Russia must pay for the massive damage caused in Ukraine and therefore calls for the Russian sovereign assets immobilised under EU sanctions to be confiscated for the purpose of supporting Ukraine's defence and reconstruction', summarising positions expressed by a majority of Members in the plenary debate held in March 2025.

Confiscation of CBR assets: Positions in different jurisdictions

The positions of EU Member States and other European countries in the confiscation debate are mixed, and are also evolving. Leaders in the UK, Poland, the Nordic countries and the Baltic states have supported, in principle, considering confiscation and have tasked legal officials with looking into the options. The largest holders of Russian assets in the EU – Belgium, France, Luxembourg and Germany – continue to oppose outright seizure, as do several other states in the euro area, such as Italy. Belgian Prime Minister Bart De Wever warned that confiscating Russian sovereign funds would amount to 'an act of war', while French President Emmanuel Macron has held that international law clearly prohibits seizure of these assets, and would only consider this measure if Moscow violates a future ceasefire or peace deal. Meanwhile, in March 2025 the French parliament passed a non-binding resolution urging the EU to appropriate frozen Russian assets and use them to support Ukraine. Beyond the EU, the positioning of the new US administration is unclear, even though there are indications that it will significantly differ from the previous open support for confiscation, while Canada has also mitigated its initial support for confiscation. Japan and Switzerland have both observed a cautious legalistic approach.

Main references

- Zaręba, S. et al., Prospect for the Use of Frozen Assets of the Central Bank of Russia, PISM, June 2025.

- International Crisis Group, A Frozen Conflict: The Dilemmas of Seizing Russia's Money for Ukraine, June 2025.

- NewLines Institute, Resolving Accountability over Russian State Assets: New Understandings of Jurisdiction and Policy Opportunities, January 2025.

- Webb, P., Legal Options for Confiscation of Russian State Assets to Support the Reconstruction of Ukraine, EPRS, European Parliament, February 2024.

Endnotes

Classification

Policy areas: Budget | Budgetary Control | Foreign Affairs | International Trade

Regions: RUSSIA

Disclaimer

This document is prepared for, and addressed to, the Members and staff of the European Parliament as background material to assist them in their parliamentary work. The content of the document is the sole responsibility of its author(s) and any opinions expressed herein should not be taken to represent an official position of the Parliament.

Copyright

© European Union.

The reuse of this document is authorised under a Creative Commons Attribution 4.0 International (CC-BY 4.0) licence.

https://creativecommons.org/licenses/by/4.0/deed.en

To use or reproduce elements that are not owned by the European Union, permission may need to be sought directly from the respective rightsholders.